Weekly Economic Snapshot: Inflation Cools Yet Consumer Sentiment Stumbles

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsWhile the ongoing government shutdown continues to delay the release of many reports, a key piece of economic data managed to break through last week. The highly anticipated Consumer Price Index (CPI) report arrived during an already positive week for the market, and its cooler-than-expected reading pushed the S&P 500 past the 6,800 milestone for the very first time. This inflation data, alongside the latest reading on consumer sentiment, offers a timely look at the current economic landscape and will play a role in the Federal Reserve’s decision at this week’s meeting.

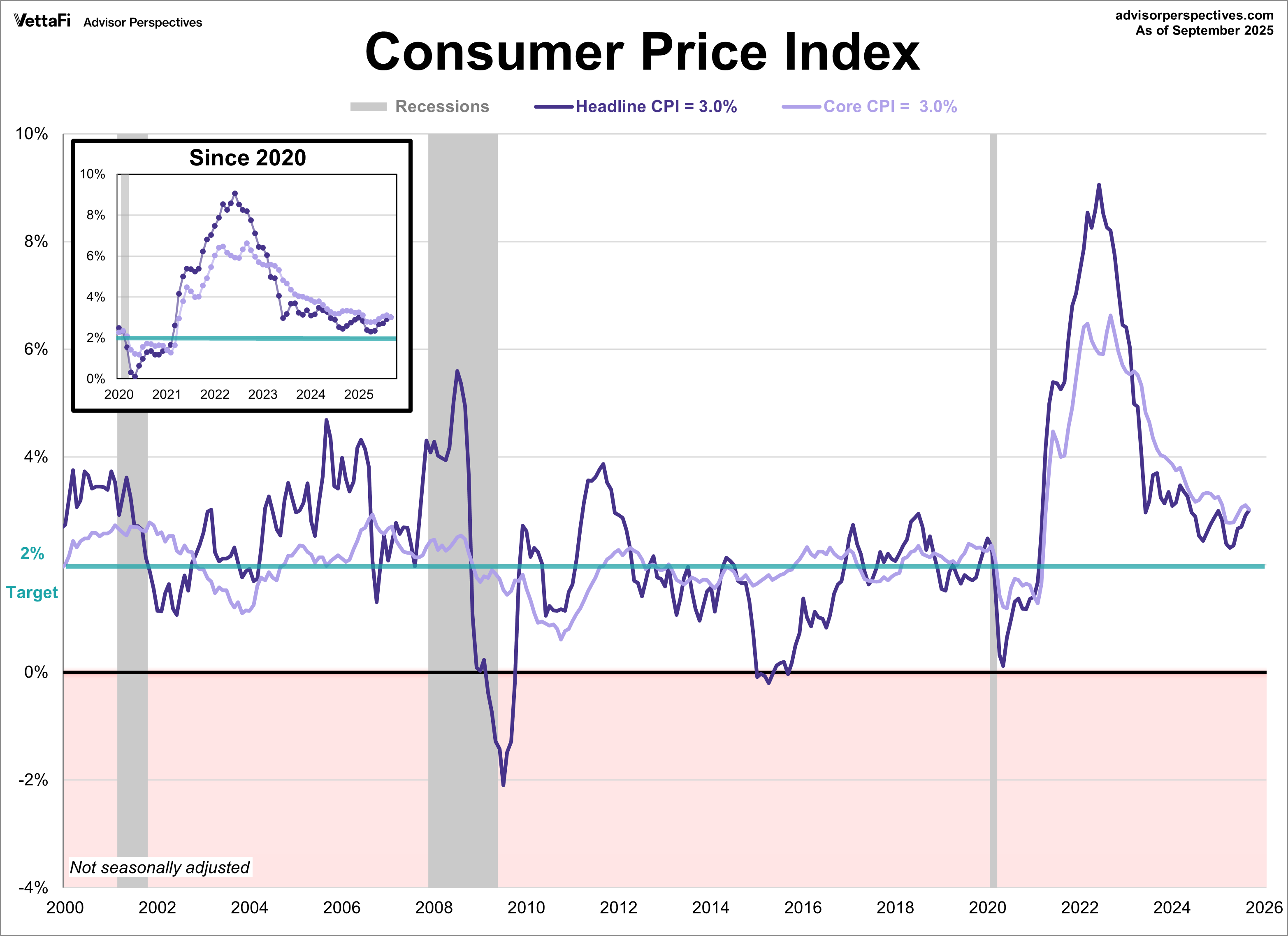

Consumer Price Index

Inflation heated up for a fifth straight month in July but came in cooler than expected in September. The Consumer Price Index (CPI) rose to 3.0%, a slight uptick from 2.9% the previous month but lower than the expected 3.1% reading. Monthly price growth also cooled, rising 0.3%. This was a deceleration from the 0.4% increase in August and was below the projected 0.4% monthly growth. Core inflation, which excludes volatile food and energy prices, cooled to 3.0% in September. This was down from 3.1% in August and below the expected 3.1% annual growth. Core prices were up 0.2% on a monthly basis, less than the projected 0.3% increase.

The largest factor for the overall CPI increase in September was higher gas prices. Furthermore, the indexes for food, shelter, airline fares, recreation, household furnishings, and apparel all saw price increases from the previous month. On the deflationary side, indexes for motor vehicle insurance, used cars, and communication costs declined.

This report is a critical piece of government data for the Federal Reserve (Fed) ahead of its interest rate decision this week. The cooler-than-expected reading will likely keep the Fed on track for an interest rate cut amid ongoing concerns surrounding the labor market.

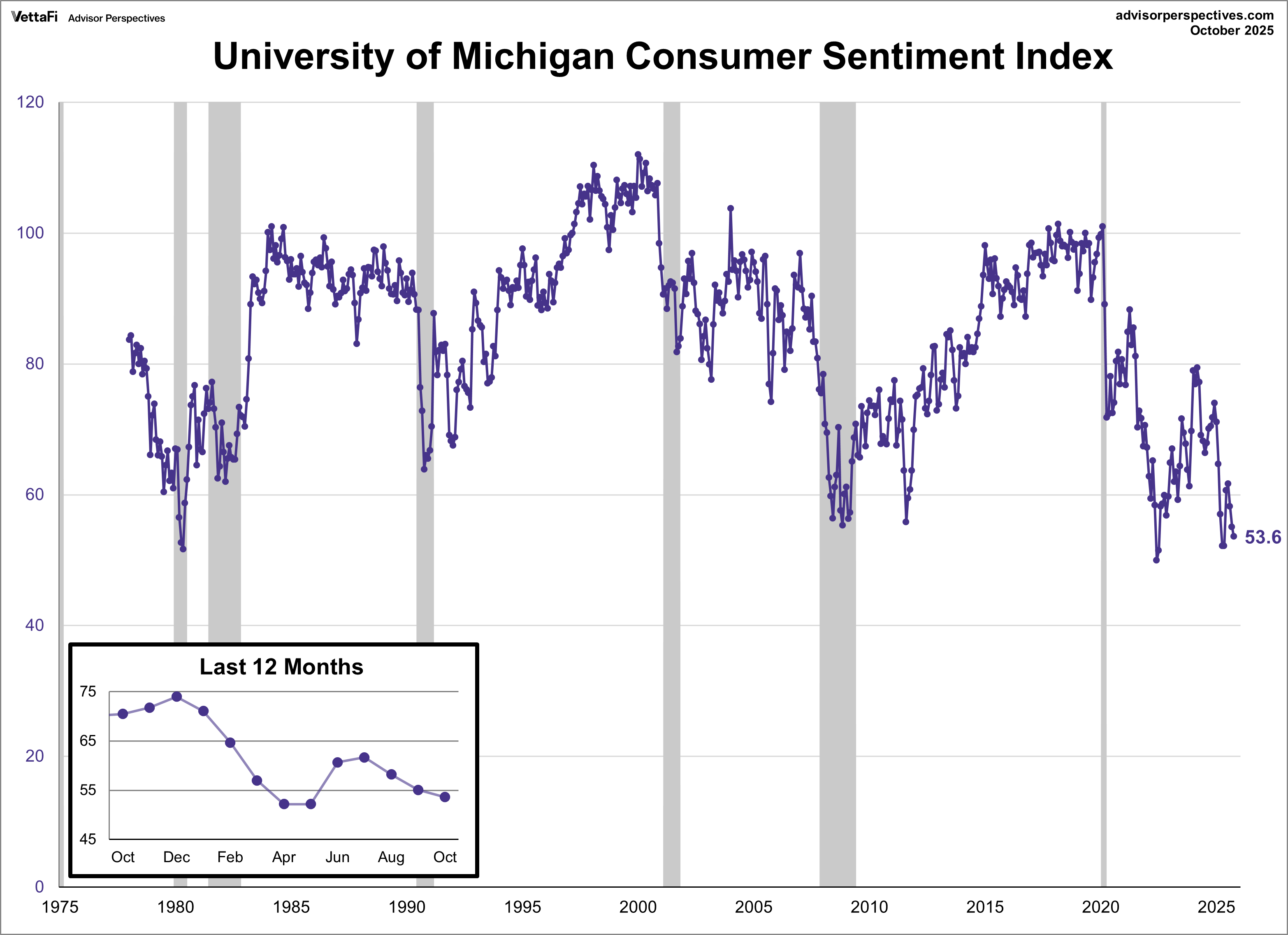

Michigan Consumer Sentiment

Consumer sentiment fell for a third straight month in October, reaching its lowest level since May. The University of Michigan Consumer Sentiment Index dropped nearly 3% to 53.6 this month, coming in below the forecast of 55.0.

The index's deterioration was largely attributed to persistent worries over inflation and high prices, with little evidence of the potential government shutdown having a significant impact. While sentiment among younger consumers improved, the overall decline was offset by noticeable drops among middle-age and older consumers. Similarly, the sub-index for current personal finances inched up, but the sub-index for future expectations retreated.

Inflation expectations for the near term eased for a second consecutive month, dropping from 4.7% in September to 4.6% in October for the year ahead. Meanwhile, long term expectations heated up for a third straight month, jumping from 3.7% to 3.% for the five-year outlook.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer sentiment.

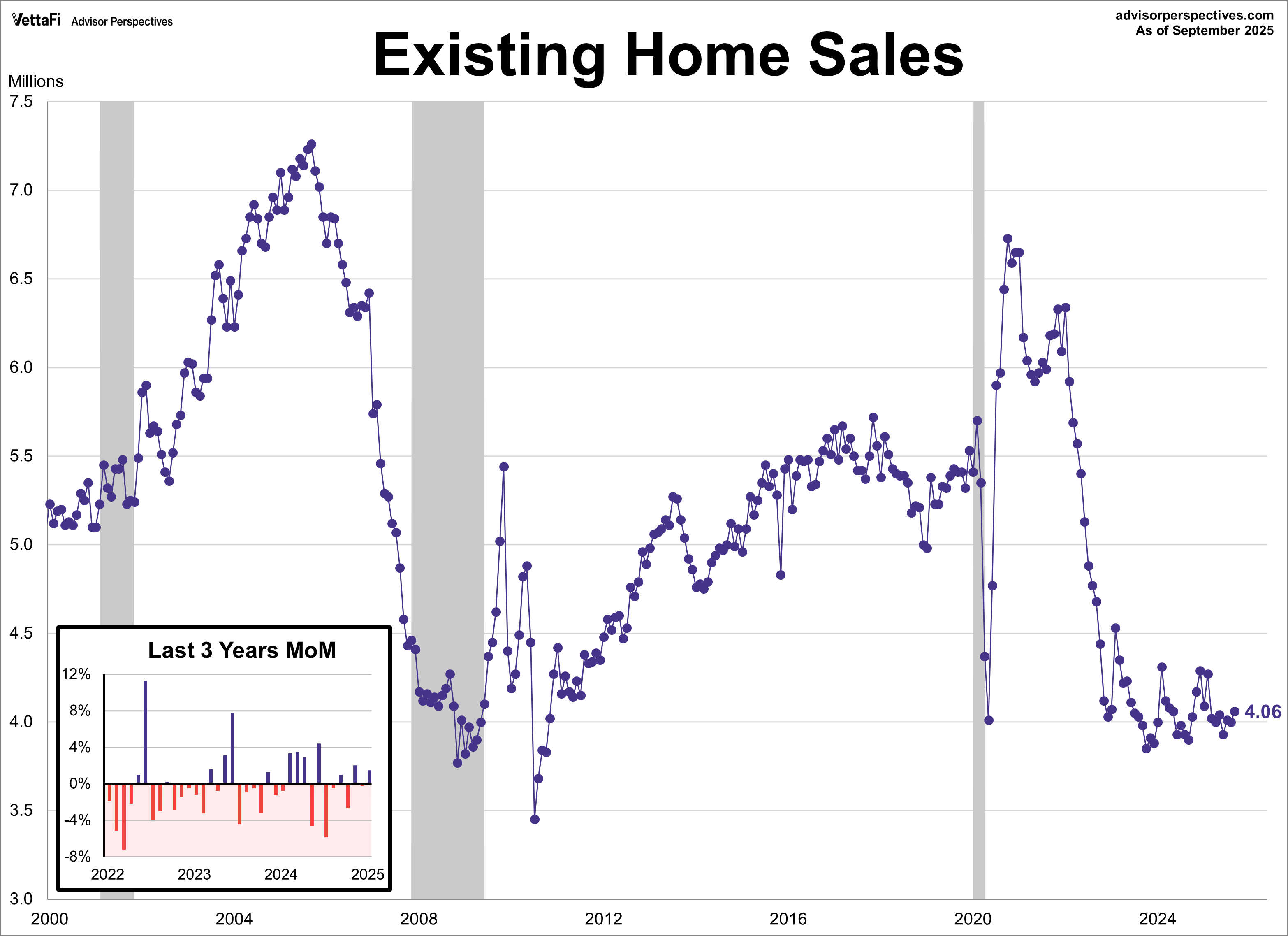

Existing Home Sales

Falling mortgage rates helped lift existing home sales to their highest level in seven months in September. Sales of previously owned homes rose 1.5% last month, reaching a seasonally adjusted annual rate of 4.06 million units, which was in line with expectations.

Declining mortgage rates, coupled with falling home prices, have helped improve housing affordability. The median price for an existing home was down for a third straight month, hitting its lowest level in five months. The median price was down 1.7% from August but up 2.1% from a year ago, marking the 27th consecutive month of year-over-year price increases.

Market Reactions

The S&P 500 briefly crossed above 6,800 for the first time in history on Friday, ultimately finishing the day at a new record high. The index posted a weekly gain of 1.9%, its third in the past four weeks. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.9% last week. Meanwhile, the S&P Equal Weight Index was up 1.7% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.7%.

The 10-year Treasury yield finished the week at 4.02%, while the 2-year note finished at 3.48%.

The CME FedWatch Tool currently shows a 97% likelihood that the Fed will cut rates by 25 basis points at their meeting this week. Markets are also pricing in another 25 basis point cut at the December meeting and three additional cuts in 2026.

Economic Data in the Week Ahead

This week’s economic outlook remains complex, given the ongoing government shutdown. Since official government data releases remain delayed, the handful of private and regional reports we do receive will be important in providing real-time insights into economic activity.

The financial world’s attention will be on the upcoming Federal Reserve meeting, where the policy decision and any accompanying statements will shape market expectations for the months ahead. Beyond the Fed, the state of the housing market will be tracked through two backward-looking price reports, the S&P Case-Shiler and FHFA Home Price Indexes, along with the forward-looking Pending Home Sales data. In the manufacturing sector, regional reports such as the Chicago PMI, the Dallas Fed Manufacturing Survey, and the Richmond Fed Manufacturing will offer some of the most current data on business conditions, hiring, and new orders for their respective regions. Finally, the Conference Board’s Consumer Confidence Index will provide another pulse check on consumer attitudes towards the economy.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Upcoming Virtual Events View All