The past few weeks felt like an economic black hole. Every month, we rely on a steady stream of official government numbers to make AP Charts and evaluate where we stand. But when the longest government shutdown in history began on October 1st, the data stream froze.

That delay created uncertainty in markets, complicated decisions for an already divided Federal Reserve, and left us wondering when AP Charts would be back on the schedule. Now that government workers are back in the office, the data flood is coming. Here are the four reports we’re most excited for, why they matter, and what we last heard from them.

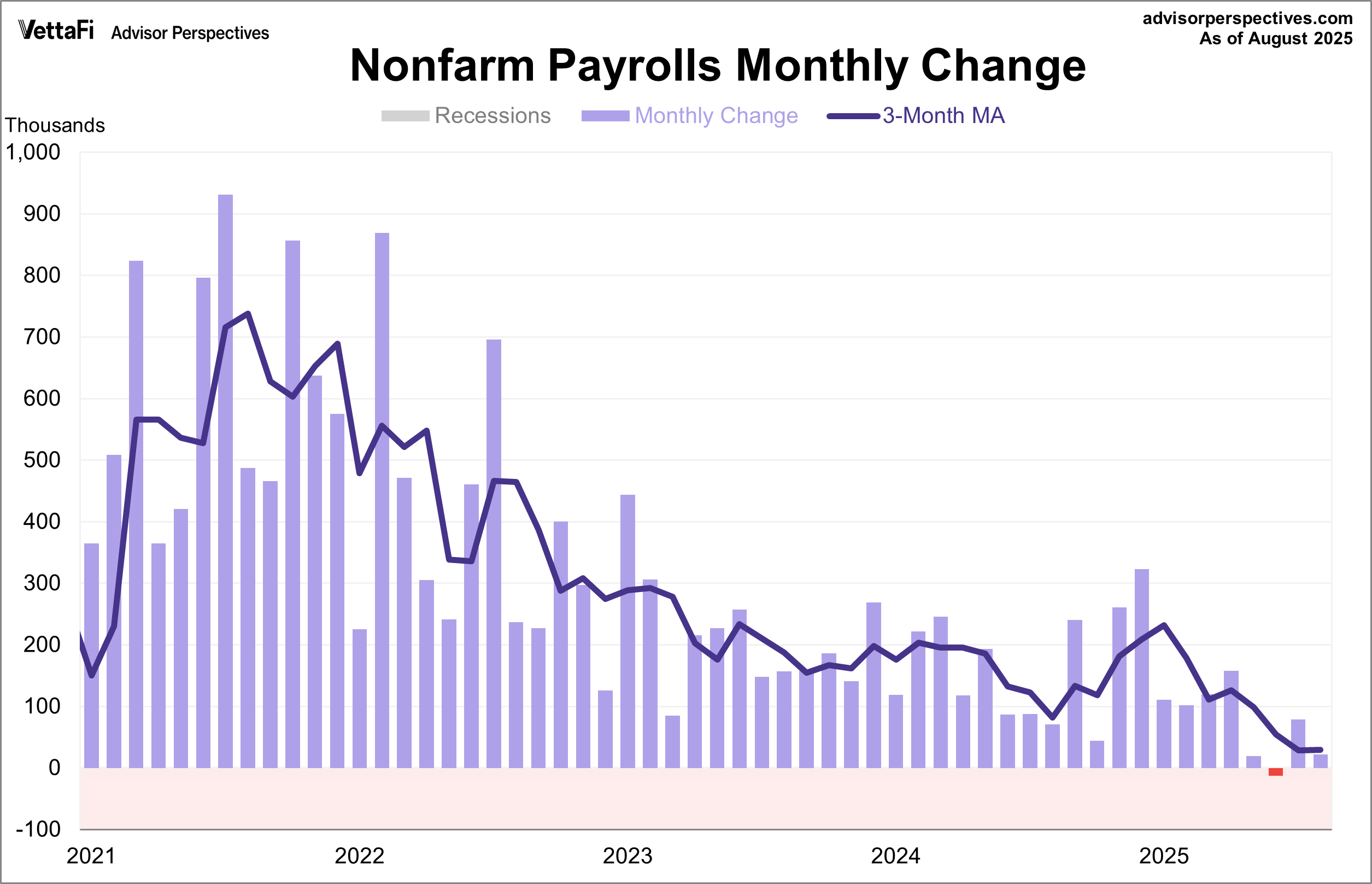

1. Employment

The monthly jobs report from the Bureau of Labor Statistics (BLS) is arguably the most watched monthly indicator. It details the current state of the labor market and household earnings, which is a major factor in forecasting future economic activity and serves as one half of the Fed’s dual mandate.

- What We Last Heard: The August jobs report saw job gains fall to 22,000, missing the 75,000 consensus and marking a sharp reversal from July. Additionally, the unemployment rate inched up to 4.3%, its highest level since 2021.

- Why We’re Excited: The labor market was already on shaky ground before the shutdown. The Fed has explicitly stated that downside risks to employment have risen recently. We’re excited to see if this slowdown has continued over the past few months, validating the Fed's decision to focus more heavily on combatting rising unemployment than rising inflation.

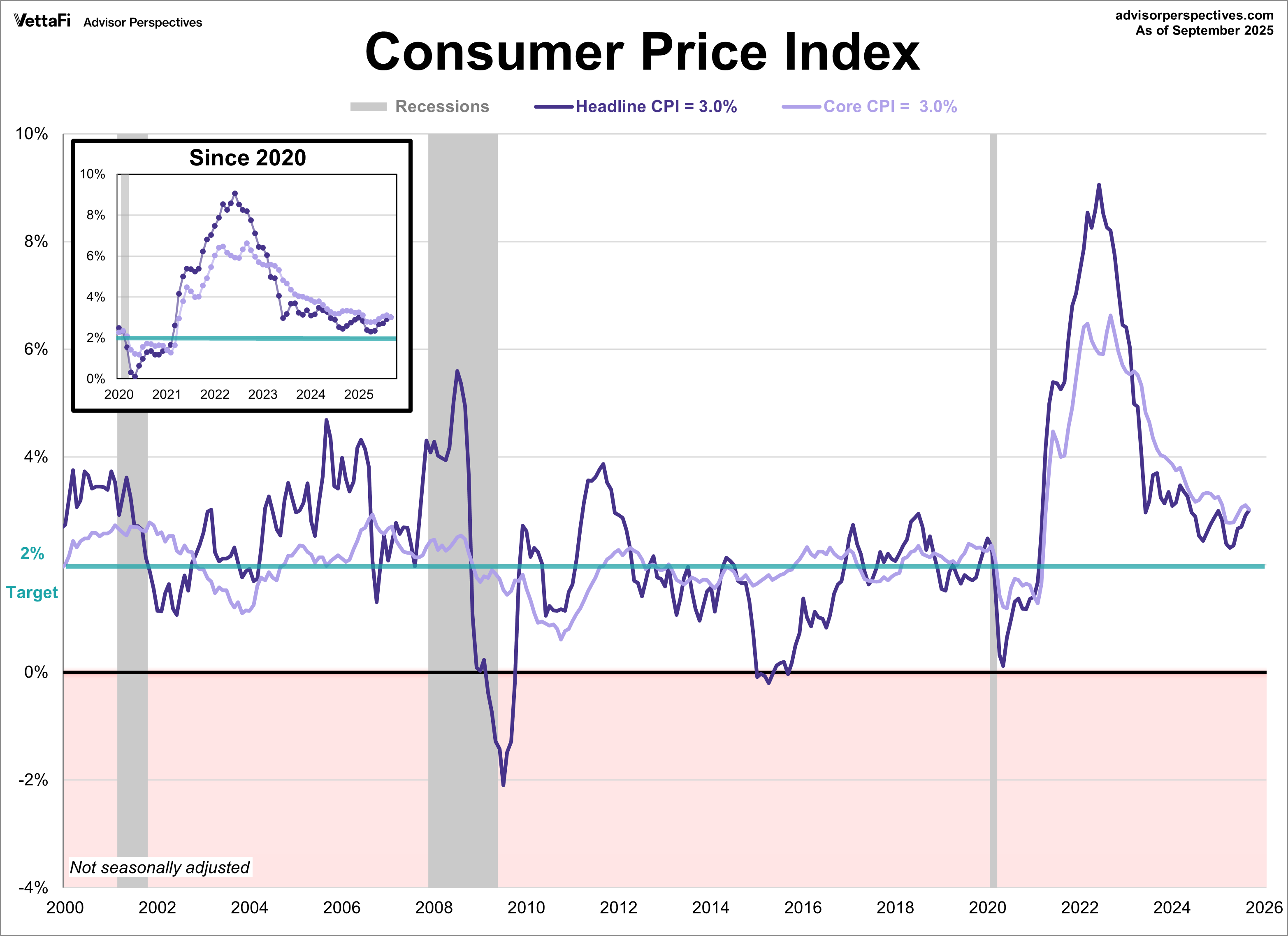

2. Inflation

The other half of the Fed’s dual mandate is price stability. While the Fed officially prefers the PCE Price Index, the Consumer Price Index (CPI) is the most recognizable to consumers and drives crucial real-world adjustments like Cost of Living Adjustments (COLAs) for social security benefits.

- What We Last Heard: The importance of this data meant CPI was the sole exception during the shutdown, allowing us to receive a delayed September report. That report showed the overall Headline CPII crept up to 3.0% year-over-year, largely due to energy costs. However, the more closely watched Core CPI, which strips out volatile food and energy, cooled to 3.0% year-over-year. Both readings came in below the expected 3.1% annual growth.

- Why We’re Excited: The most recent data showed that headline inflation had heated up for five straight months. We’re interested to see if price pressures are finally easing, especially in major categories like housing, which accounts for a significant portion of the index. However, it’s still up in the air if we’ll ever receive the October CPI report. Without it, the Fed remains at a disadvantage going into their next meeting.

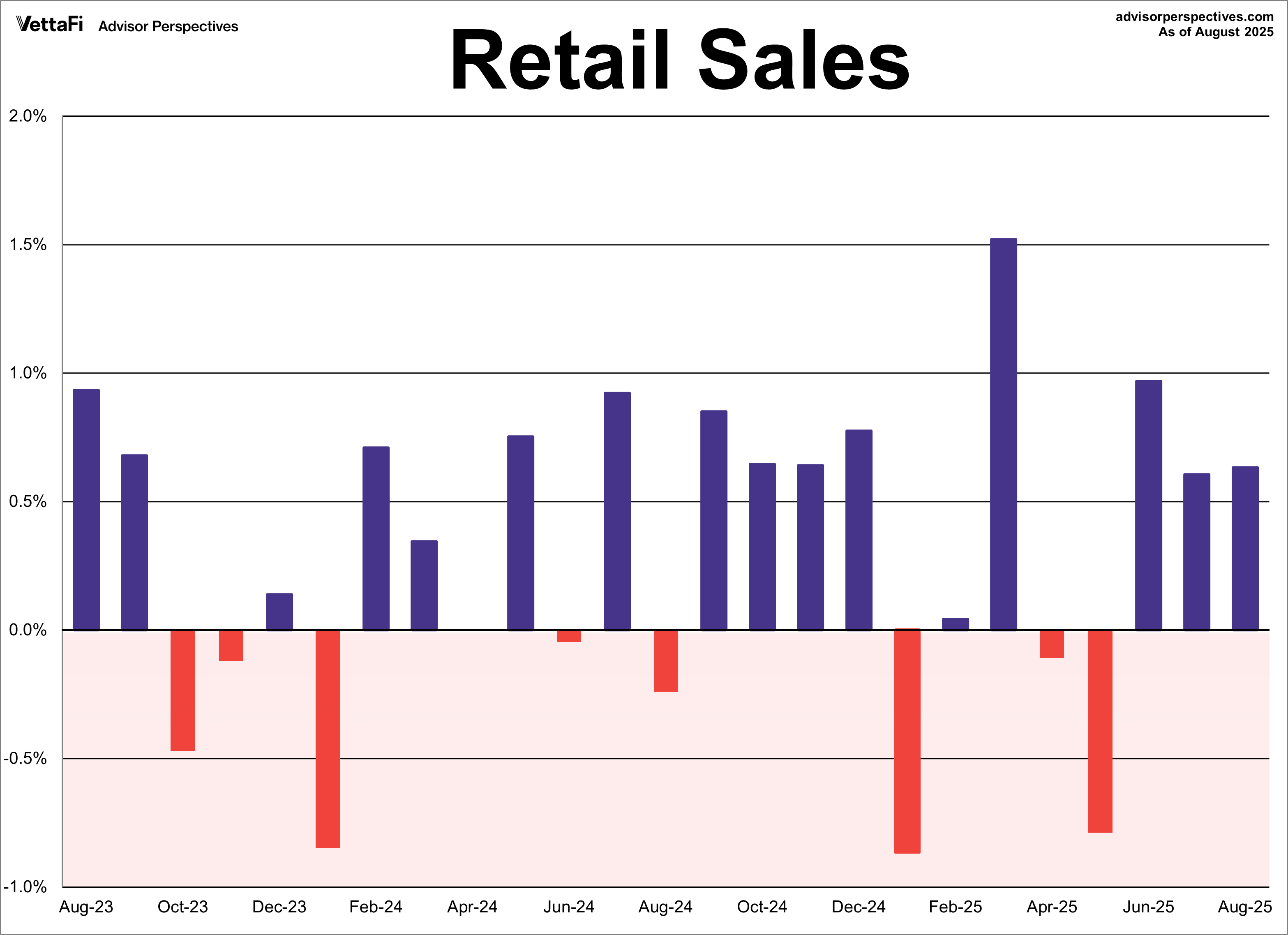

3. Retail Sales

This report measures how much stuff consumers actually bought. Since consumer spending is the engine powering roughly 70% of the economy, with retail sales accounting for nearly one-third of that, it is the best indicator we have for measuring shifts in spending patterns.

- What We Last Heard: Headline retail sales blew past expectations in August, rising 0.6% month-over-month versus the anticipated 0.2%. This marked the third consecutive monthly increase, with July’s number revised upward, signaling underlying momentum.

- Why We’re Excited: The resilient U.S. consumer is the primary reason the forecast recession never arrived. But that resilience is cracking: credit card debt is at an all-time high, and savings are dwindling. Furthermore, spending is driven mostly by the wealthy, exacerbating the K-shaped economy. We’re interested to see if that lower-income half of the 'K' has finally given up, because a negative print signals deep consumer trouble heading into the holidays.

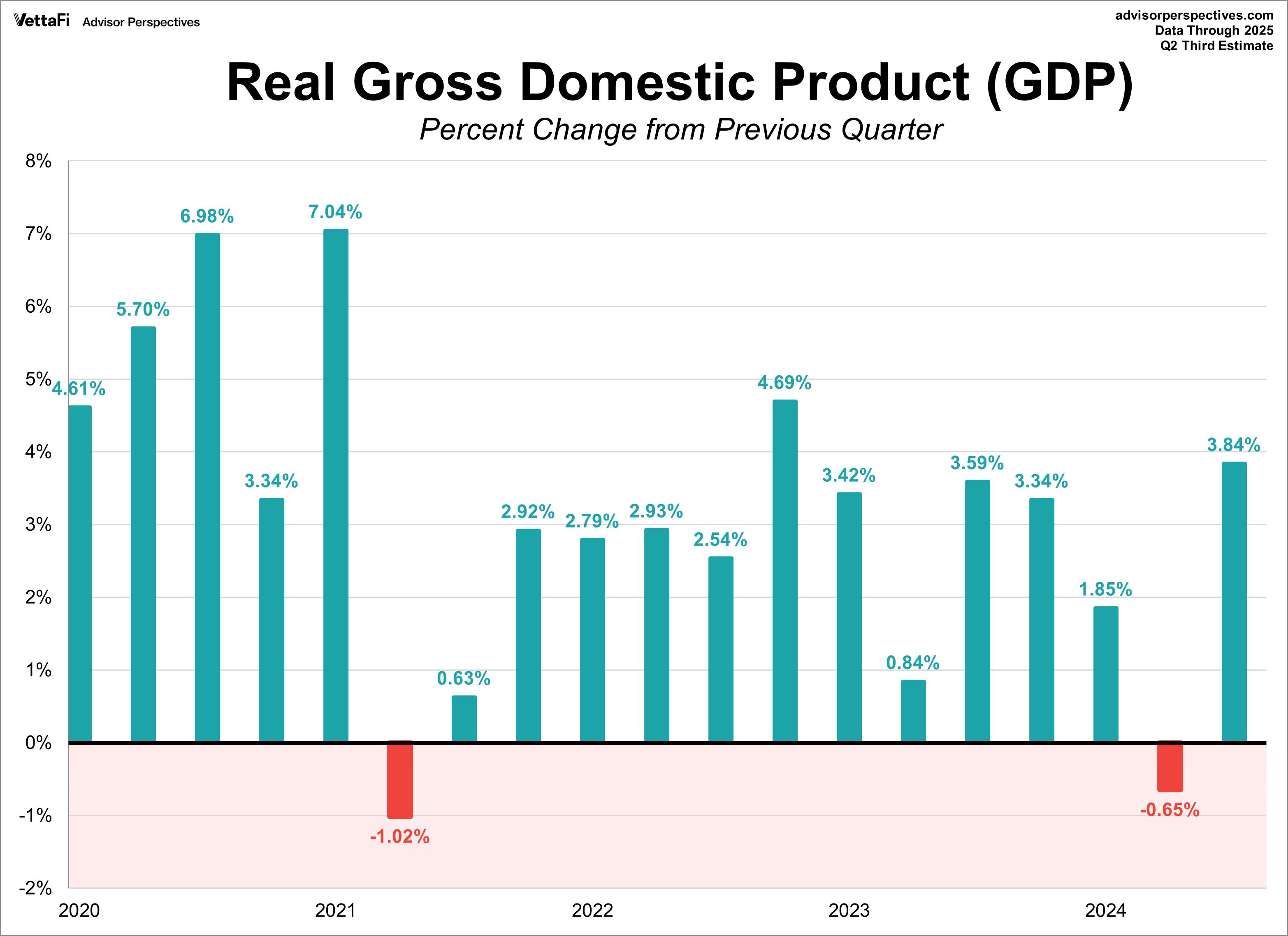

4. Gross Domestic Product (GDP)

This is the quarter-over-quarter summary of economic activity, often considered the most important statistic to come out each quarter. Although GDP is a lagging indicator, it helps to confirm the trend we’ve been guessing at.

- What We Last Heard: The U.S. economy expanded in the second quarter, with real GDP increasing at an annual rate of 3.8%. This was higher than the forecast of 3.3% and marked a significant turnaround from Q1’s -0.6% contraction.

- Why We’re Excited: The economy bounced back in the second quarter, but we’ve yet to see if that strength continued in Q3. We’re interested in seeing the first estimate for the third quarter because we’ll have a gauge of how much momentum the economy had before the shutdown began.

Reading the Tea Leaves: What the Private Data Suggested

The good news is that not all data collection halted during the shutdown. Private companies and non-government agencies kept reporting, providing a little bit of light through the blackout. However, these proxies paint a weak forecast for our missing reports.

- ADP Employment: This private payroll report served as our leading labor market indicator. We saw a loss of 29,000 private jobs in September followed by a gain of 42,000 in October. While the month-to-month figures between ADP and the official BLS report are famously unreliable, this sharp slowdown in private hiring is a major red flag that is hard to ignore as we await the larger nonfarm payrolls data.

- PMI Data (Manufacturing/Services): The Purchasing Managers’ Indexes (PMIs) from ISM provide insight on sentiment and activity. The recent reports showed the manufacturing sector continuing its long contraction. While the services sector returned to expansion territory, a hidden detail within the services PMI showed the employment subindex contracted, providing another worrying signal for the broader labor market.

- Consumer Attitudes: Surveys from the University of Michigan (Sentiment) and The Conference Board (Confidence) have indicated that consumers are growing increasingly pessimistic about the overall economy. Because consumer spending is the single largest component of the economy, this attitude shift is alarming. When people worry about their jobs and the economy, they’ll pull back on discretionary purchases which could signal trouble for the forthcoming Retail Sales and GDP reports.

Our Main Takeaway: Fed Policy is Now Reactionary

The Federal Reserve has repeatedly stated they are data-dependent, yet at their latest meeting, they were forced to make decisions without the most crucial information. This has left policymakers “flying blind” for the past several weeks. While several data points will come out before their December meeting, the Fed will still be operating under a data gap, yet again being forced to make decisions with incomplete information.

Our main takeaway? The government shutdown has forced the Fed and markets into a reactionary stance. Instead of being able to carefully analyze a steady stream of indicators, we're being forced to cram six weeks of economic learning into a much shorter timeframe.

We are playing catch up on economic reports and as a result playing catch up on policy. And with a Fed that already has dissenting opinions and was criticized for taking action too late to fight rising inflation back in 2022, this delay increases the risk of a policy error for a committee in no position to make mistakes.

We’re excited to have AP Charts back but the next several weeks will be a whirlwind as the market, investors, businesses, and policymakers try to quickly absorb the missing data.