Weekly Economic Snapshot: Rate Cut Meets Conflicting Jobs Data

The economic narrative last week was shaped by a highly anticipated Federal Reserve rate cut, which came against a backdrop of conflicting signals in the labor market. While the latest JOLTS report indicated job openings were rising, other data pointed toward a clear softening of the broader labor market environment. Following the Fed's decision, the S&P 500 index initially saw a major boost, eventually crossing the 6,900 mark for the first time ever to set a new all-time high. However, that upward momentum was not sustained, with the index selling off sharply on Friday, ultimately finishing the week with a slight loss.

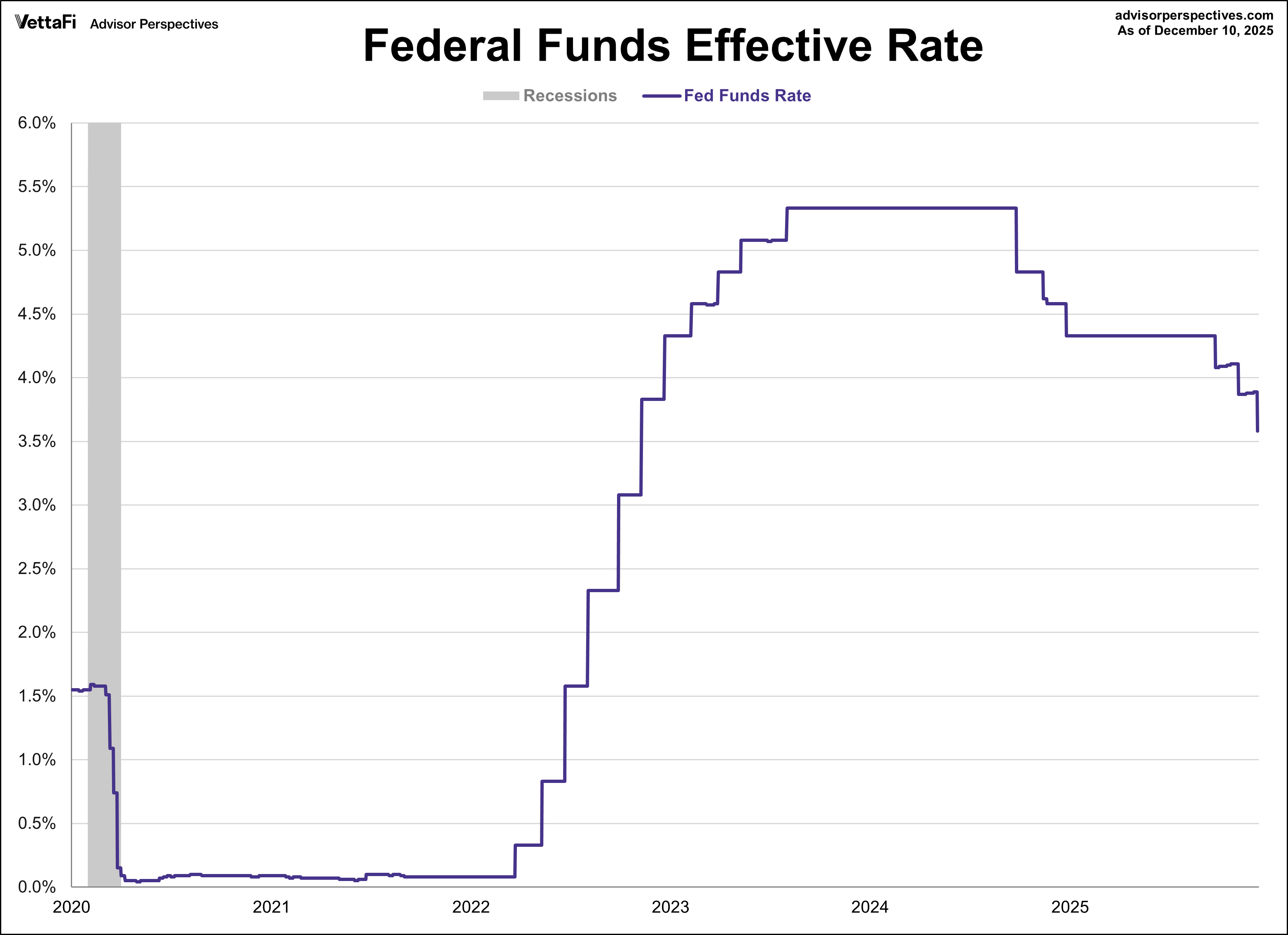

Federal Reserve Meeting: December 10, 2025

The Federal Reserve implemented a widely anticipated 25 basis point rate cut last week, adjusting the federal funds rate to a new range of 3.50-3.75%. This marks the third consecutive rate reduction and places the central bank’s target at its lowest level since November 2022. Once again, this decision came under unique circumstances, as the lingering effects of the government shutdown continued to delay or omit economic reports.

While the move was highly expected, Fed Chair Jerome Powell described the decision as a “close call.” The 9-3 vote reflected clear dissent, with two members favoring no cut and one member pushing for a 50 basis point reduction. This split highlights that some policymakers view the threat of unemployment as a greater risk than inflation, though all members appear to agree each outcome carries risk. Powell stated that the committee is now in a good position to wait and observe how things evolve. The CME FedWatch Tool currently indicates a 76% likelihood that the Fed will hold rates steady at their next meeting, compared to a 24% likelihood of a 25 basis point cut. Markets are currently projecting two 25 basis point cuts for 2026, double the Fed’s official dot plot projection of one.

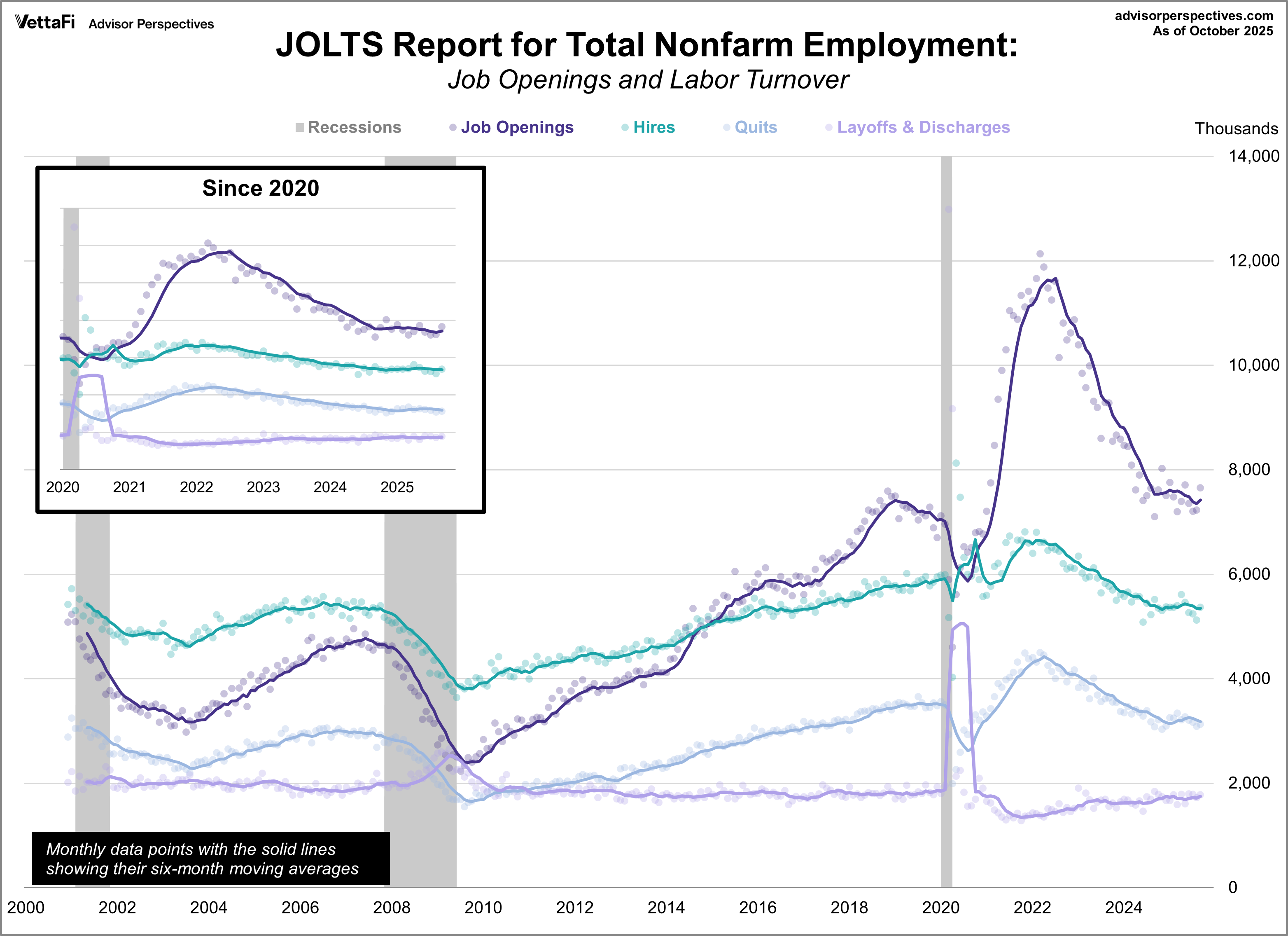

Job Openings and Labor Turnover Summary (JOLTS)

Job Openings and Labor Turnover Summary (JOLTS)

Job openings rose for a third straight month in October, according to the latest JOLTS report, which included delayed September data. Openings reached a total of 7.670 million, the highest level since May, driven by an initial surge of 431,000 from August to September and a further rise of 12,000 in October.

Meanwhile, other labor market metrics added to the narrative of a softening labor market that has been prevalent for much of the year. Hires and quits both saw their largest monthly drop in over a year, with the quits rate falling to its lowest level since 2020. Additionally, layoffs rose for a second straight month, reaching their highest level since January 2023. This “low hire, increased fire” environment clearly reflects worker caution and reduced voluntary turnover.

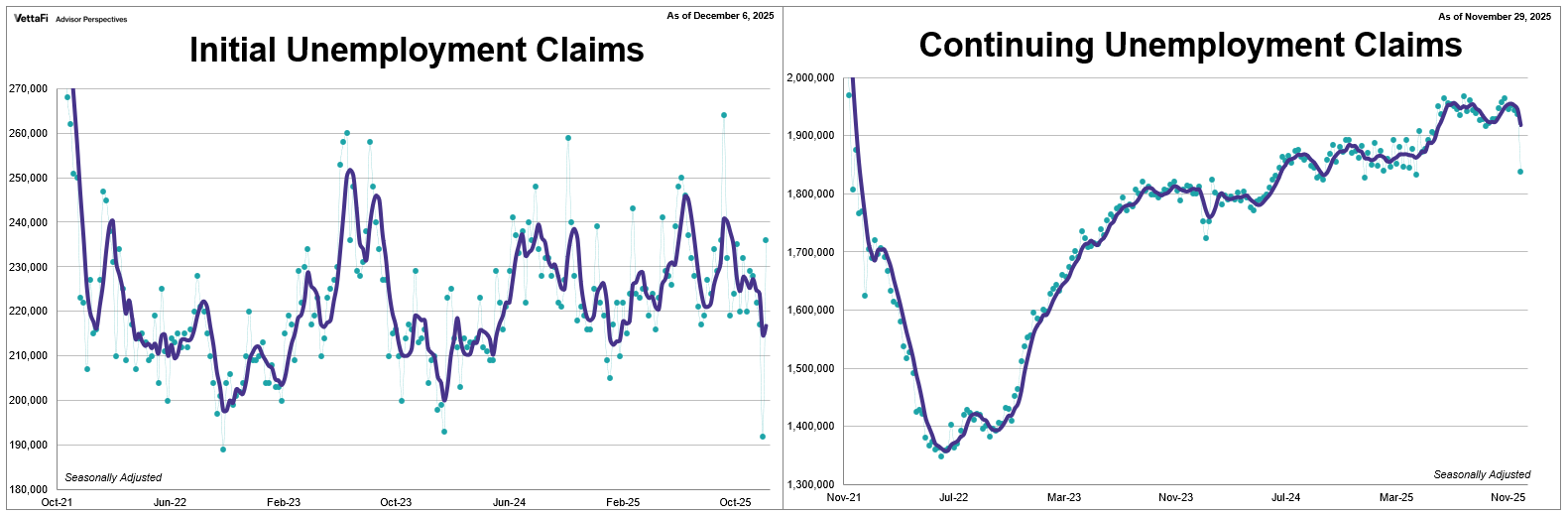

Weekly Unemployment Claims

The number of people who filed for unemployment for the first time jumped to its highest level in three months. Initial jobless claims increased by 44,000 from the previous week’s figure to 236,000, its largest weekly rise in over four years. The latest reading, with data through December 6th, was significantly higher than the forecast of 220,000.

Meanwhile, the number of people who had already filed for unemployment and continued to claim benefits fell to its lowest level in eight months. Continuing jobless claims dropped by 99,000 to 1.838 million, its largest weekly decline in four years. The latest reading, with data through November 29th, was lower than the 1.950 million forecast.

Jobless claims data is typically volatile around the holiday season. Therefore, despite the latest extreme numbers, it is important to consider this seasonal trend.

Market Reactions

The S&P 500 reached a new record high this week, crossing the 6,900 milestone for the first time ever. However, the index experienced its largest daily loss in three weeks on Friday, ultimately leading to a weekly loss of 0.6%. As a result, the SPDR S&P 500 ETF Trust (SPY) fell 0.6% last week. Meanwhile, the S&P Equal Weight Index was up 0.7% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.8%.

The 10-year Treasury yield finished the week at 4.19%, while the 2-year note finished at 3.52%.

Economic Data in the Week Ahead

The economic schedule for the week ahead is congested due to the recent government shutdown, forcing key reports onto an unusual timeline. The week’s primary highlights are concentrated in the job market, consumer spending, and inflation. Tuesday will deliver a combined view of the economy with the BLS Jobs Report for November and the delayed October Retail Sales report. Focus then shifts to inflation on Thursday with the Consumer Price Index (CPI) for November, before concluding Friday with the final reading of the Michigan Consumer Sentiment Index.

Other updates throughout the week will provide crucial sector-specific insights, including regional manufacturing surveys along with housing data from the NAHB Housing Market Index and Existing Home Sales.