Weekly Economic Snapshot: Labor Strength Meets Cooling Inflation

The U.S. economy began 2026 with a display of unexpected resilience in the labor market, even as long-term data revisions painted a more modest picture of 2025 growth. While consumer spending showed signs of exhaustion during the holiday season, inflation continued its downward trajectory, reaching levels not seen in several years. These cooling price pressures, paired with a stabilizing labor market, have solidified expectations that the Federal Reserve will maintain its current rate stance through the first quarter.

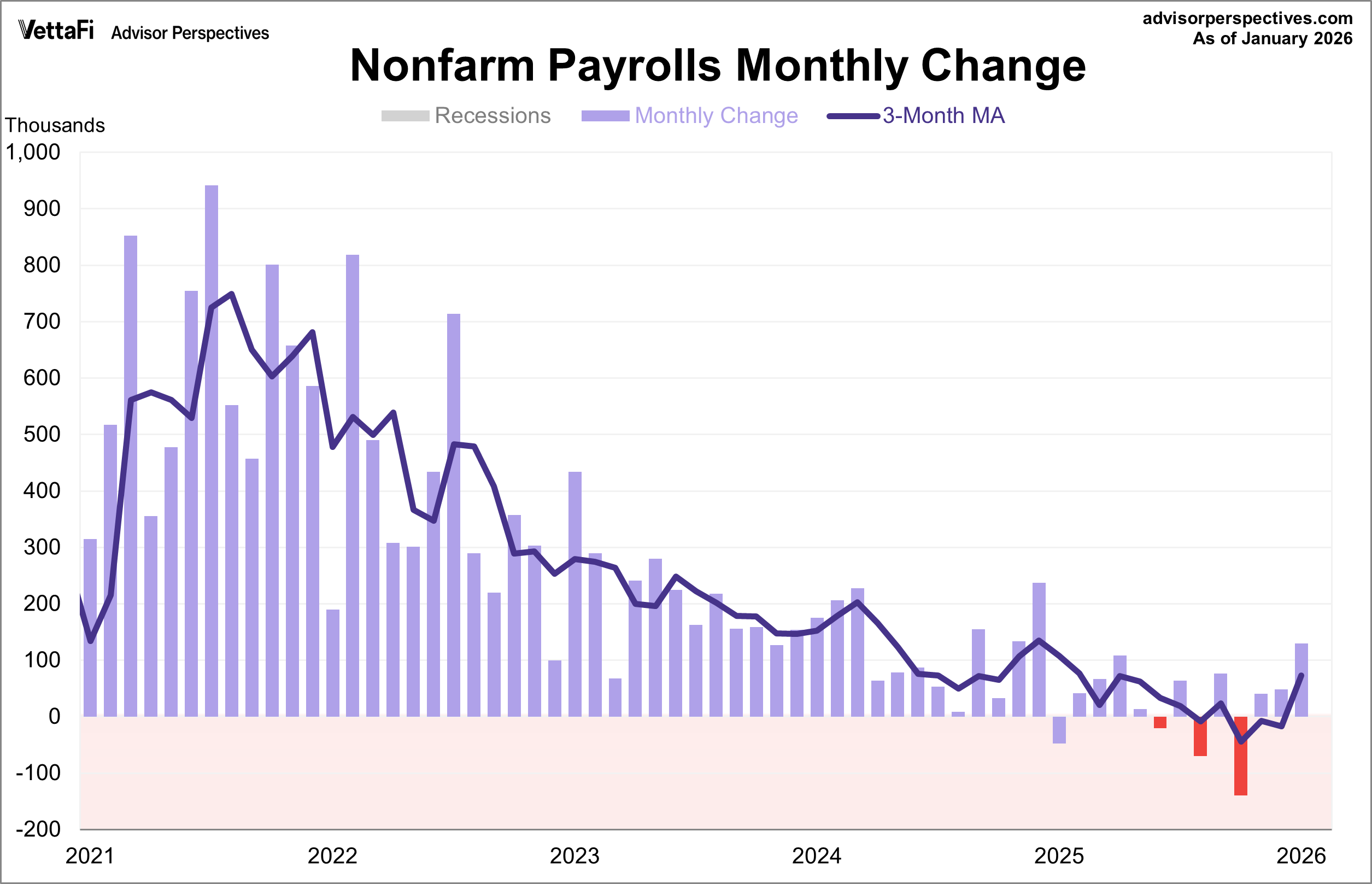

Employment: Unexpected Strength

The January employment report revealed a labor market that was significantly stronger than anticipated to start the year. The U.S. economy added 130,000 jobs last month, exceeding the projected 48,000 additions and marking the largest growth since late 2024. Additionally, the unemployment rate edged down to 4.3%.

However, the report also included sobering revisions for the previous year. Data now shows the economy added only 181,000 jobs in 2025, a sharp downward revision from the initial estimate of 584,000. For the Federal Reserve, this mix of current strength and past stabilization likely justifies a "wait-and-see" approach regarding future rate cuts.

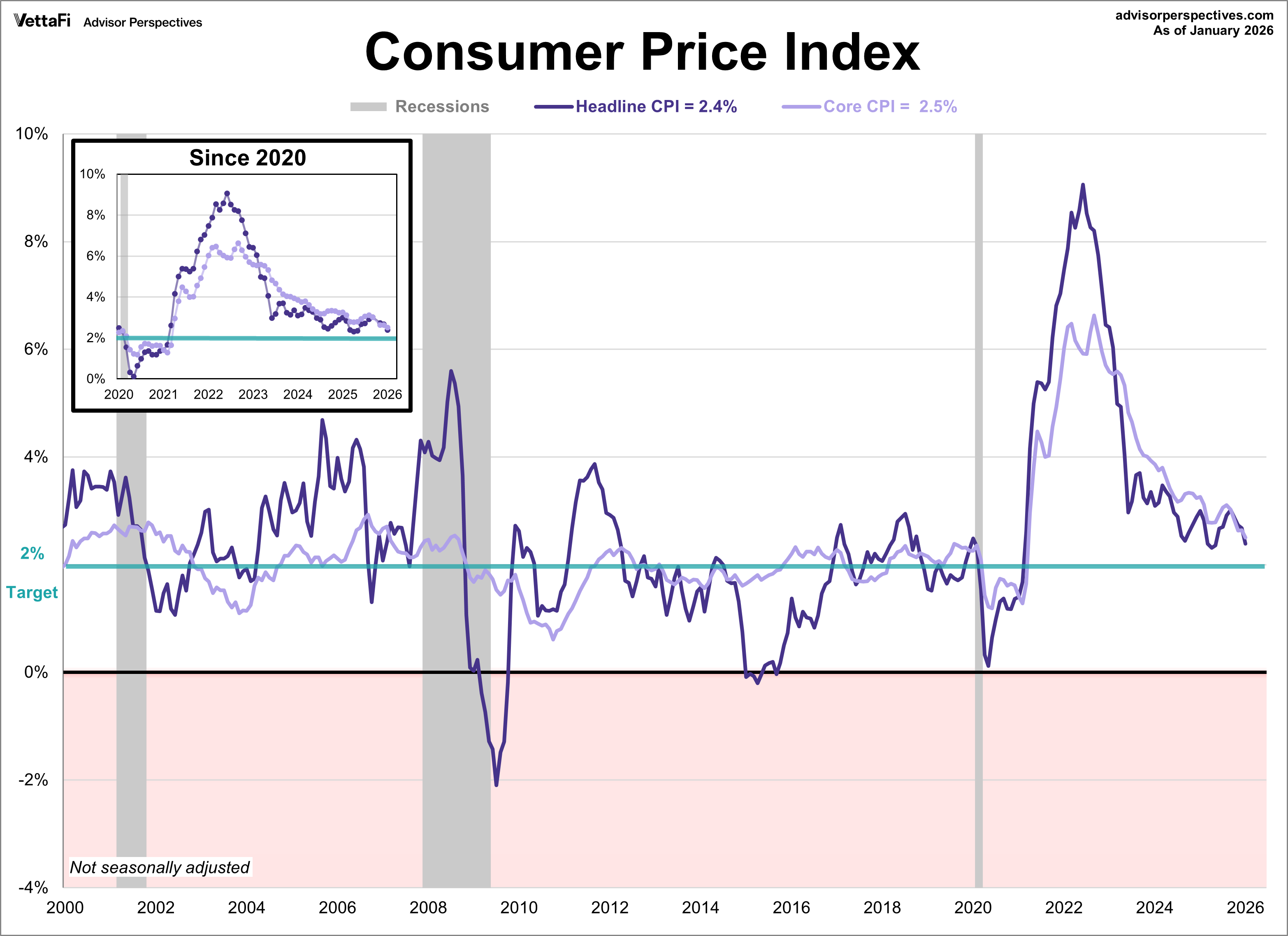

Inflation: Cooling Continues

Consumer inflation cooled for a third straight month in January, reaching its lowest level since May. The Consumer Price Index (CPI) came in at 2.4% last month, down from 2.7% in December and lower than the expected 2.5% annual growth. On a monthly basis, prices were up 0.2%, less than the expected 0.3% growth. Core inflation, which excludes volatile food and energy, eased to 2.5%, its lowest level since 2021. Additionally, core prices were up 0.2% from the previous month. Both readings were consistent with their respective forecasts.

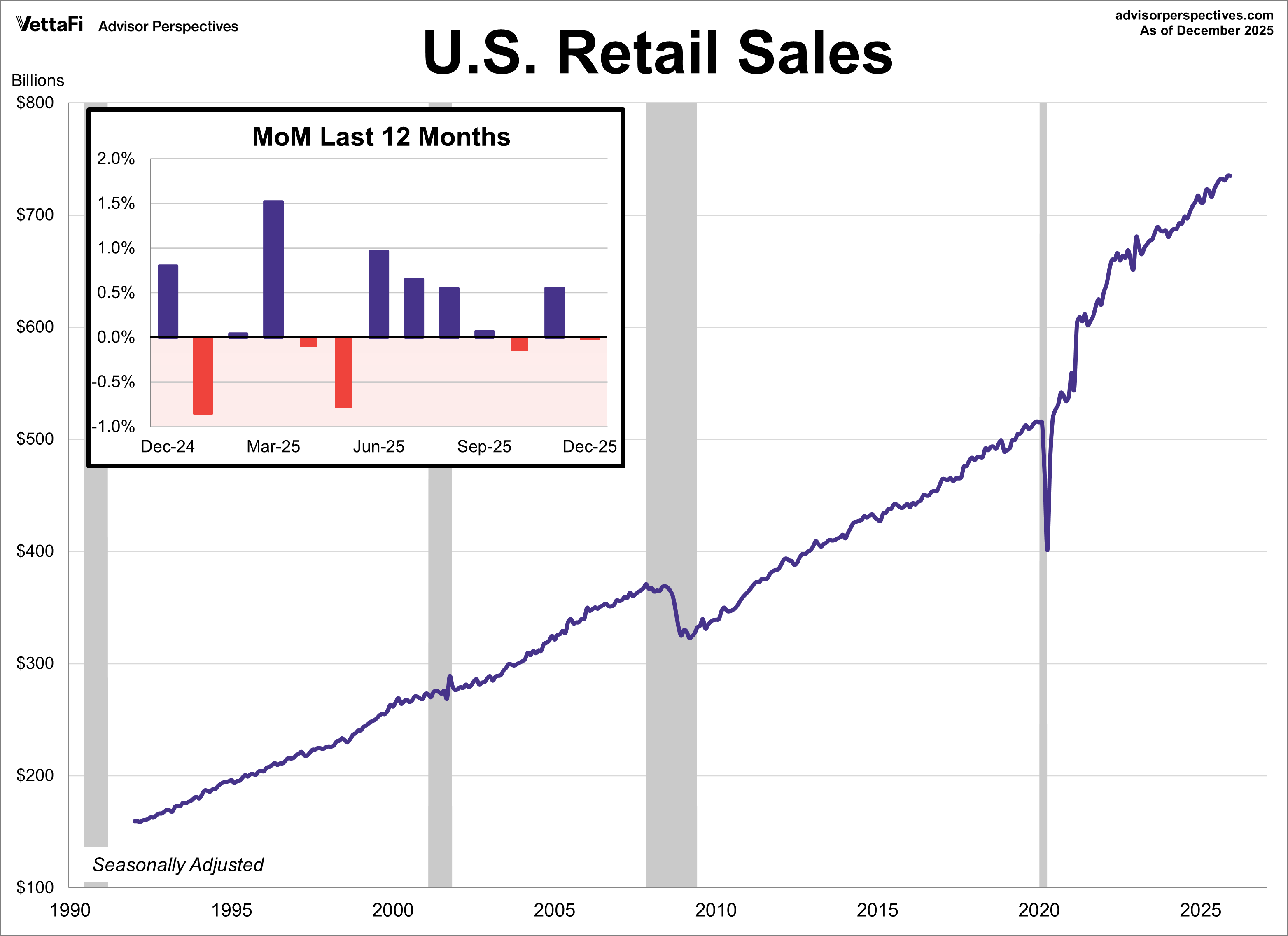

Retail Sales: Consumer Fatigue Sets In

Despite the holiday season, consumer spending was unexpectedly muted in December. Retail sales were flat for the month, missing the 0.4% growth projection and marking a sharp downturn from December’s 0.6% reading.

Core sales, which exclude autos, were also lower than expected, coming in nearly flat against the expected 0.3% growth. Lastly, control purchases, a crucial GDP input and an even more “core” view of retail sales, came in below expectations with a -0.1% decline, falling short of the 0.4% growth forecast.

Retail sales could impact the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

Market Reactions

The S&P 500 finished the week with a loss of -1.4%, its second consecutive weekly decline. This was largely driven by a selloff on Thursday, sparked by concerns related to AI. As a result, the SPDR S&P 500 ETF Trust (SPY) fell -1.3% last week. Meanwhile, the S&P Equal Weight Index was up 0.3% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 0.3%.

The 10-year Treasury yield finished the week at 4.04%, its lowest level since November. Meanwhile the 2-year note finished at 3.40%, its lowest level since 2022.

The CME FedWatch Tool currently shows a 90% chance the Fed will hold rates steady at their next meeting in March. Markets are pricing in two 25 basis point cuts in 2026, coming at the June and September meetings, with an additional cut in 2027.

Economic Data in the Week Ahead

- Monday: Holiday - no data

- Tuesday: NY Empire State Manufacturing Index (Feb), NAHB Housing Market Index (Feb)

- Wednesday: Durable Goods (Dec), Housing Starts (Dec), Building Permits (Dec), Industrial Production (Jan)

- Thursday: Weekly Jobless Claims, Philadelphia Fed Manufacturing Index Feb), Trade Balance (Dec), Pending Home Sales (Jan)

- Friday: GDP (Q4 Advance Estimate), PCE Price Index (Dec), New Home Sales (Dec), University of Michigan Consumer Sentiment Index (Feb)