Daily Pricing Is Not Daily Liquidity

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsKey takeaways:

- Daily pricing is not price discovery. Producing a daily price mark using model-based inputs is simply a higher-frequency version of the same process that already generates wide dispersion among prices of comparable assets. Without market-clearing transactions to anchor valuations, the result is more noise rather than more accuracy.

- The core issue is observability, not frequency. Price marks diverge because managers use different assumptions and no one is required to transact at the stated price. Until that changes, dispersion will persist regardless of how often valuations are updated.

- True secondary market liquidity faces formidable structural barriers, and the more achievable near-term fix is better governance. Independent valuation agents, standardized methodologies, and tighter oversight can narrow dispersion meaningfully – but not completely eliminate it.

Within private credit, attempts to increase liquidity – the ability to buy or sell an asset quickly, in size, and at prices reflecting fundamental values – are welcome developments, in our view. Yet until these efforts address the market’s inherent structural constraints, including a lack of true price discovery, they will only increase the perception of liquidity without truly improving liquidity.

Read more: U.S. Inflation Measures Tell Two Different Stories

The debate over daily pricing in private credit portfolios has evolved from a narrow accounting question into a proposed remedy for the market’s dispersed – and often stale – valuations. Two related developments have driven this shift.

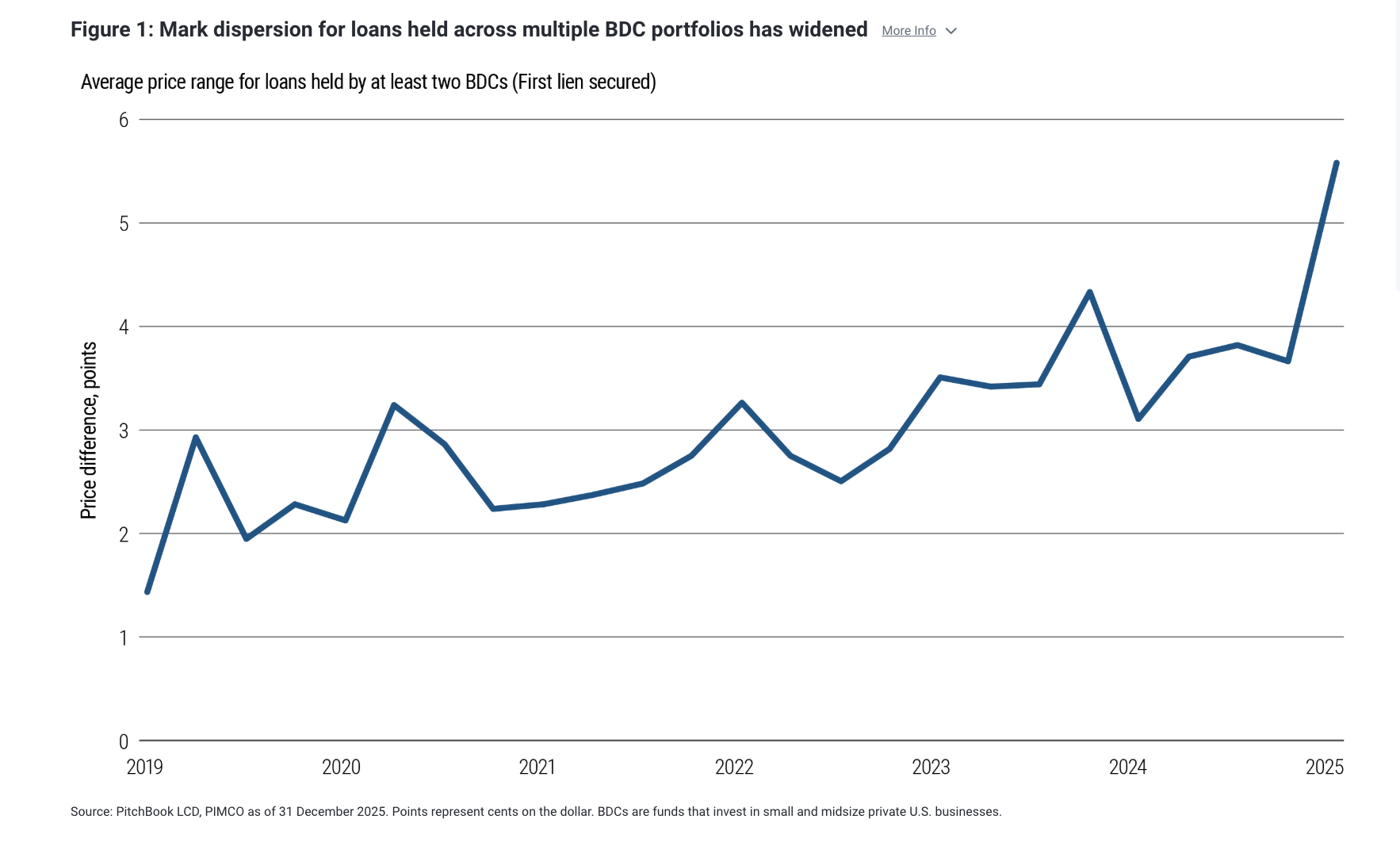

First, price mark dispersion for loans held across multiple business development company (BDC) portfolios has widened sharply in recent quarters. By year-end 2025, marks for the same instrument were, on average, about five points apart (see Figure 1). These gaps are difficult to reconcile with the notion of arm’s-length fair value determinations for identical assets.

To be sure, some dispersion is inevitable under the Financial Accounting Standards Board’s (FASB) Level 3 accounting, where managers have latitude over assumptions, discount rates, and comparables. But the magnitude of recent dispersion suggests that the absence of observable transactions is no longer a benign feature of the market.

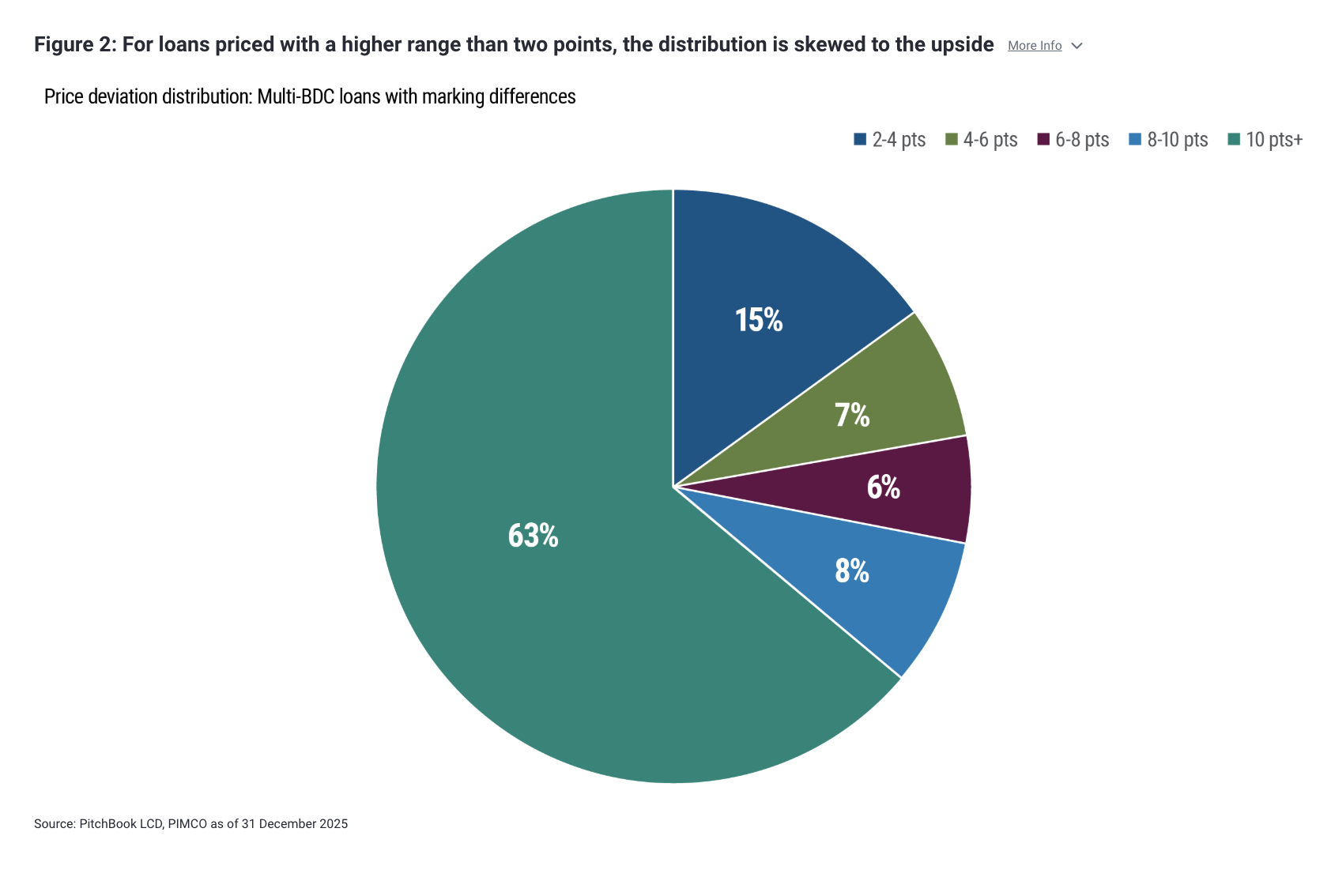

In some cases, reported net asset values (NAVs) appear to reflect managers’ views more than market-clearing values. For context, we estimate that 83% of loans held by at least two BDCs are priced within a two-point range; for the remaining 17%, the distribution is notably skewed to the upside (see Figure 2).

More frequent pricing is not more accurate pricing

Daily pricing is not only an incomplete answer to these issues – it may even exacerbate them. Daily pricing is not price discovery. At best, it adds marginal transparency and some reputational pressure that may rein in the most extreme mark outliers. But on its own, it is not a meaningful structural reform of the private credit market.

Any manager can produce a daily price estimate using an imputation model based on discount rates, comparable spreads, and borrower-level credit metrics. But that is simply a higher-frequency application of the same Level 3 valuation process that already produces wide dispersion in quarterly BDC marks.

The same loan can be marked five or even 10 points apart because managers are not anchoring valuations to the same inputs, and, more importantly, because no one is required to transact at the stated price. If three BDCs rely on different model inputs on a quarterly basis, they will do so daily as well. The result would be dispersion at a higher frequency, potentially with more noise, not less. The core problem, therefore, is not frequency. It is methodology and observability.

Why true price discovery in private credit remains a high bar

Broadly speaking, there are two pathways to address valuation dispersion and stale marks in private credit. The first is incremental and more immediately attainable: greater reliance on third-party validation, independent valuation agents, standardized methodologies, and tighter governance, which would help narrow differences in how assets are priced across managers. The second is more transformative: genuine transaction-based price discovery anchored in a functioning secondary market.

The distinction matters. Third-party validation can improve consistency, but it does not fully resolve the core issue; these marks are still, at their foundation, model-driven rather than market-cleared. True price discovery requires observable transactions and continuous two-way flow.

Yet the bar for achieving that outcome is significantly higher than commonly assumed. Even setting aside the fact that many participants have limited economic incentives to promote liquidity in their own assets, several structural constraints would need to be addressed:

- Standardization of instruments and data. Private credit lacks the common language that underpins liquidity in public markets, including standardized identifiers, consistent documentation, and uniform financial reporting. This fragmentation limits comparability across assets and makes it difficult for participants to underwrite trades at scale. Without a credible foundation for benchmarking and relative value analysis, secondary activity risks remaining episodic and bespoke, more akin to a balance sheet management tool than a true market.

- Settlement and operational infrastructure. While discussions often gravitate toward electronic trading platforms or TRACE-like reporting, the more immediate constraint is far more basic: settlement. Today’s trade settlement processes are slow, manual, and operationally intensive. Until settlement becomes faster, more predictable, and scalable, turnover will remain inherently constrained. In other words, trading velocity is less a function of pricing transparency than of post-trade frictions.

- Transferability constraints. Many private credit agreements retain borrower consent provisions for loan transfers. This introduces a fundamental friction with no real public-market equivalent. In practice, it creates uncertainty around execution timelines and transfer certainty, two conditions that are essential for any market seeking to support regular, institutional trading activity.

- Information asymmetry and conflicts of interest. The information barriers facing secondary buyers in private credit go well beyond deal documentation. Access to borrower-level data is often gated by non-disclosure agreements (NDAs), and disclosure frameworks are neither standardized nor continuous. But even where some price transparency exists – such as occasional bid-offer indications – those quotes are frequently sourced from affiliates of the originator or the manager itself. This introduces a structural conflict of interest: The entity providing the price signal may also be the party with the greatest economic stake in where that asset is marked. For a secondary market to function credibly, pricing needs to be not just available but transparent, independent, and objective. Without that, participants cannot distinguish between genuine market-clearing levels and marks that serve the commercial interests of the price-setter. This is the inverse of the regime that supports public credit liquidity, where broad, independent dissemination of information underpins confidence in both pricing and transaction costs.

- Limited structural sponsorship for two‑way secondary flow. Sustainable liquidity is ultimately a function of consistent two-way flow. The evolution of the broadly syndicated loan market is instructive: Liquidity deepened materially as collateralized loan obligations (CLOs) and ETFs created a durable, programmatic bid. Private credit lacks an equivalent demand engine at scale. While middle market CLOs have grown, the ecosystem remains nascent and insufficient to anchor a continuous secondary market. Absent that, trading activity is likely to remain opportunistic rather than structural.

In the absence of true liquidity, look for an illiquidity premium

Efforts to improve pricing accuracy in private markets will need to address fundamental issues of transparency, objectivity, and the lack of market-based transactions and price discovery. Given these hurdles will continue to persist, we believe it’s unlikely that any meaningful convergence in liquidity will be achieved between private and public markets. With that in mind, investors in private markets should remain focused on receiving adequate compensation, including a premium for illiquidity and credit quality differences.

Disclosures

Statements concerning financial market trends or portfolio strategies are based on current market conditions, which will fluctuate. There is no guarantee that these investment strategies will work under all market conditions or are appropriate for all investors and each investor should evaluate their ability to invest for the long term, especially during periods of downturn in the market. Outlook and strategies are subject to change without notice.

Charts are provided for illustrative purposes and are not indicative of the past or future performance of any PIMCO product. Forecasts, estimates and certain information contained herein are based upon proprietary research and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. There is no guarantee that results will be achieved.

Past performance is not a guarantee or a reliable indicator of future results. References to specific securities and their issuers are not intended and should not be interpreted as recommendations to purchase, sell or hold such securities. PIMCO products and strategies may or may not include the securities referenced and, if such securities are included, no representation is being made that such securities will continue to be included.

All Investments contain risk and may lose value. An investment in a BDC is subject to credit and investment risk, leverage risk, market and valuation risk, price volatility risk, liquidity risk, interest rate risk and structural and regulatory risk. Private credit involves an investment in non-publicly traded securities which may be subject to illiquidity risk. Portfolios that invest in private credit may be leveraged and may engage in speculative investment practices that increase the risk of investment loss.

PIMCO as a general matter provides services to qualified institutions, financial intermediaries and institutional investors. Individual investors should contact their own financial professional to determine the most appropriate investment options for their financial situation. This material contains the opinions of the author and such opinions are subject to change without notice. This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product. Information contained herein has been obtained from sources believed to be reliable, but not guaranteed. No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission. PIMCO is a trademark of Allianz Asset Management of America LLC in the United States and throughout the world.

CMR2026-0508-5475424

A message from Advisor Perspectives and VettaFi: Discover something new! Click here to register for our upcoming webcasts.

© PIMCO

Membership required

Membership is now required to use this feature. To learn more:

View Membership Benefits