Chart-ing the Economy: Week of August 11th - 15th

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsLast week, the S&P 500 experienced a rally that took it to three consecutive record highs but the momentum cooled as economic data painted a complex picture. The Consumer Price Index (CPI) showed headline inflation holding steady, providing a brief moment of relief. However, a much hotter-than-expected Producer Price Index (PPI) later in the week highlighted mounting inflationary pressures in the pipeline. This mixed inflation signal led to a shift in rate-cut expectations, pushing hopes for a larger cut at the next FOMC meeting back toward a more modest 25 basis points. Meanwhile, even as consumer sentiment fell for the first time in four months amid rising inflation worries, consumer spending remained resilient.

Inflation

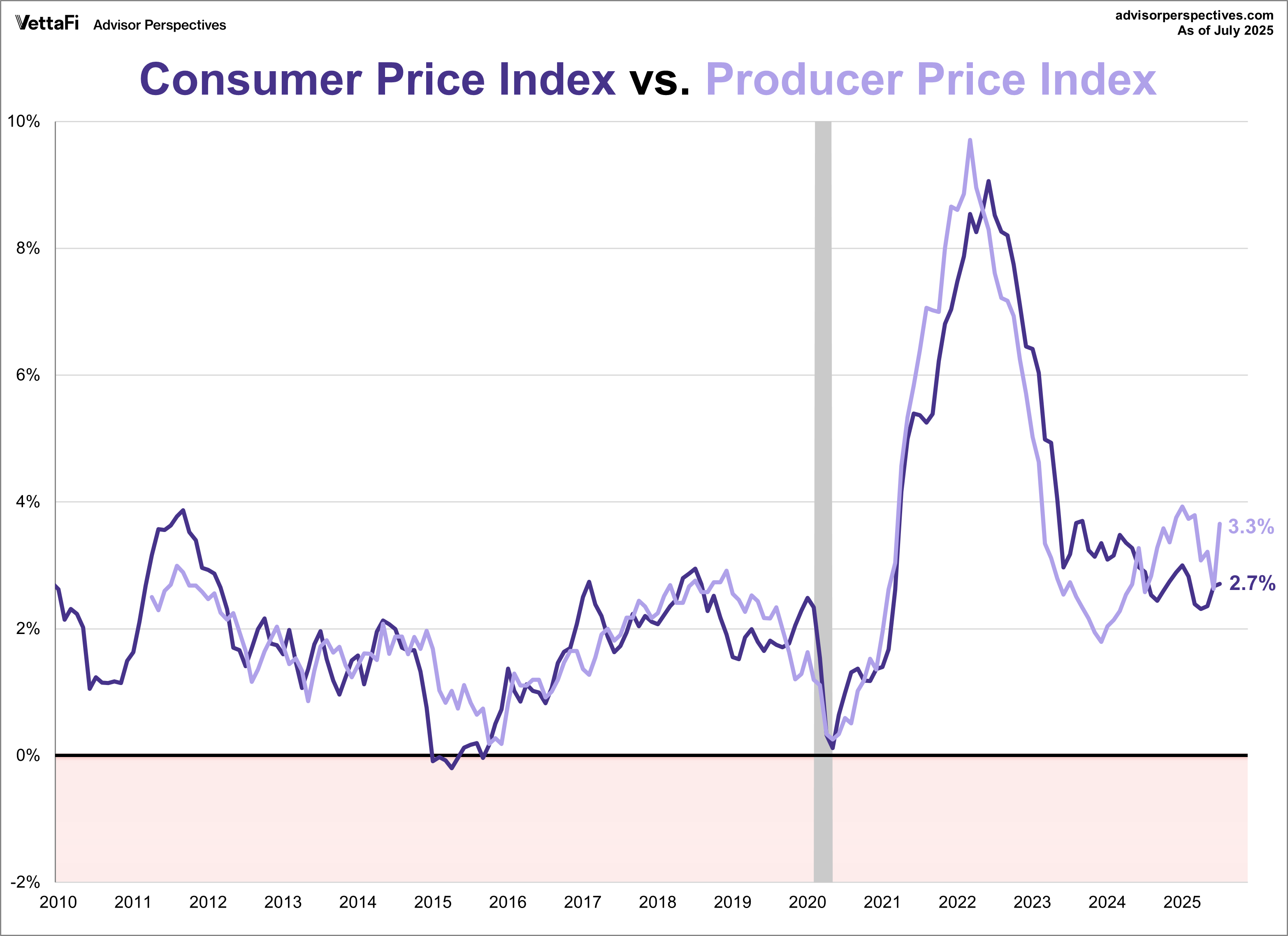

Consumer inflation held steady in July, with the Consumer Price Index (CPI) remaining unchanged at 2.7%, below the expected 2.8% annual growth. On a monthly basis, prices were up 0.2%, as expected. Core inflation, which excludes volatile food and energy, rose to 3.1%, up from 2.9% in June and above the 3.0% forecast. On a monthly basis, core prices were up 0.3%, as expected.

However, business-side inflation told a different story, as the Producer Price Index (PPI) came in much hotter than expected in July. The index surged 0.9%, its largest monthly increase in over three years and well above the 0.2% forecast. On an annual basis, wholesale prices rose 3.3%, a five-month high that surpassed the expected 2.5% growth.

The PPI is considered a leading indicator of consumer inflation, as rising costs for producers can eventually get passed on to consumers. While recent CPI reports showed consumer prices had been slow to rise, the latest PPI data is a clear warning sign that future increases may be on the way.

Consumer Sentiment

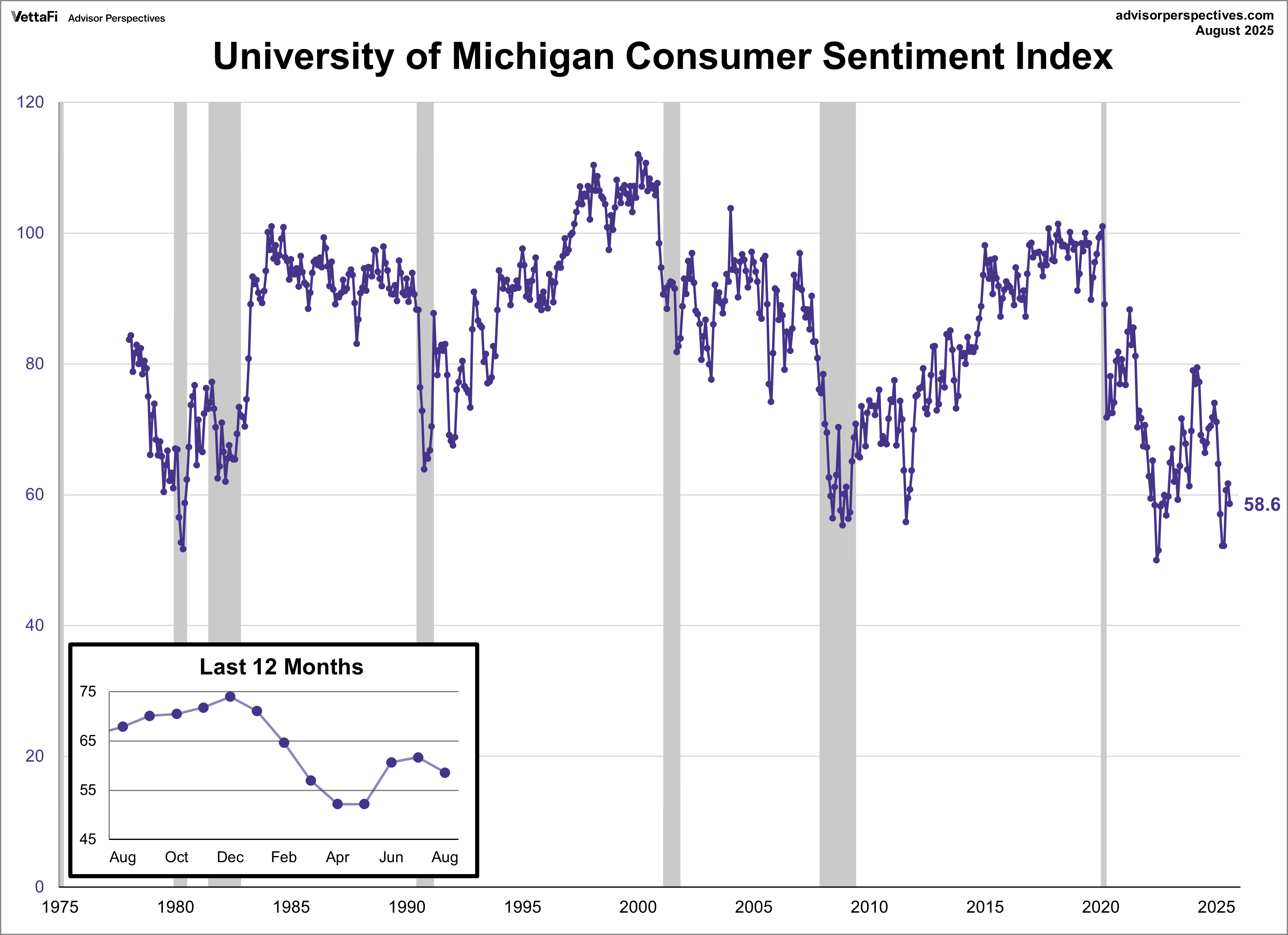

Consumer sentiment fell for the first time in four months, with the University of Michigan Consumer Sentiment Index falling 5.0% to 58.6. The latest number was lower than the expected 61.9 reading.

The index’s deterioration this month was driven by inflation concerns which consumers anticipate will continue alongside worsening unemployment. Inflation expectations rose for both the near and long term, ending two and three consecutive months of easing, respectively. Year-ahead expectations increased from 4.5% to 4.9%, while the five-year outlook rose from 3.4% to 3.9%.

Retail Sales

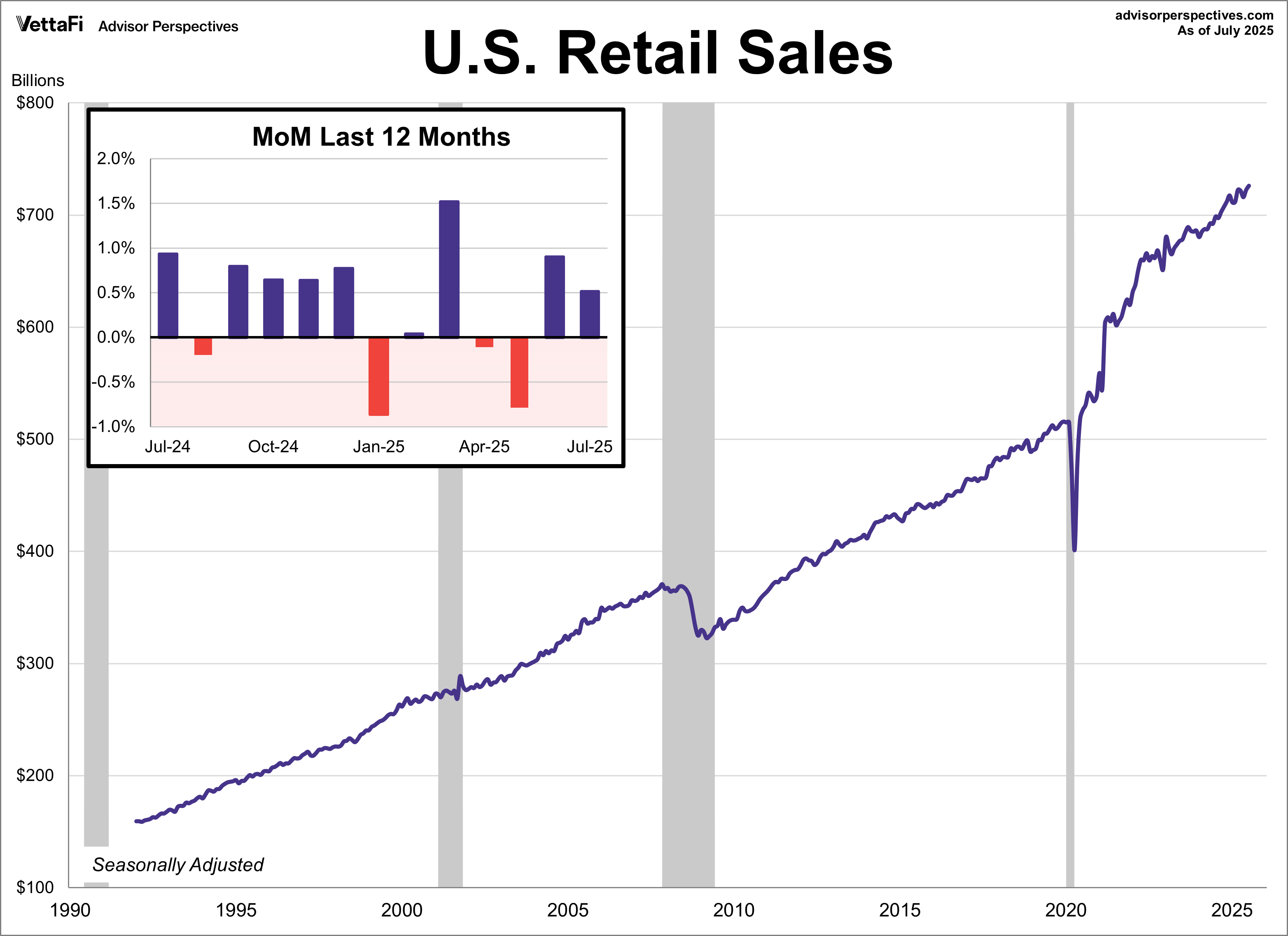

Consumer spending rose for a second straight month in July, though slightly lower than expected. Retail sales were up 0.5%, just below the 0.6% forecast. The data was bolstered by a significant upward revision to June's figure, which went from 0.6% to 0.9%, highlighting steady spending after a couple of months of pullbacks.

The increase was broad-based, with strong gains at motor vehicle dealers, furniture stores, and e-commerce platforms. However, spending declined at building material and garden stores, as well as at restaurants and bars.

Core sales, which exclude autos, were up 0.3% as expected. More encouragingly, control purchases, a crucial GDP input and an even more “core” view of retail sales, beat expectations with a 0.5% rise, surpassing the 0.4% forecast.

Retail sales could impact the SPDR S&P Retail ETF (XRT), VanEck Retail ETF (RTH), Amplify Online Retail ETF (IBUY), and ProShares Online Retail ETF (ONLN).

Market Reactions

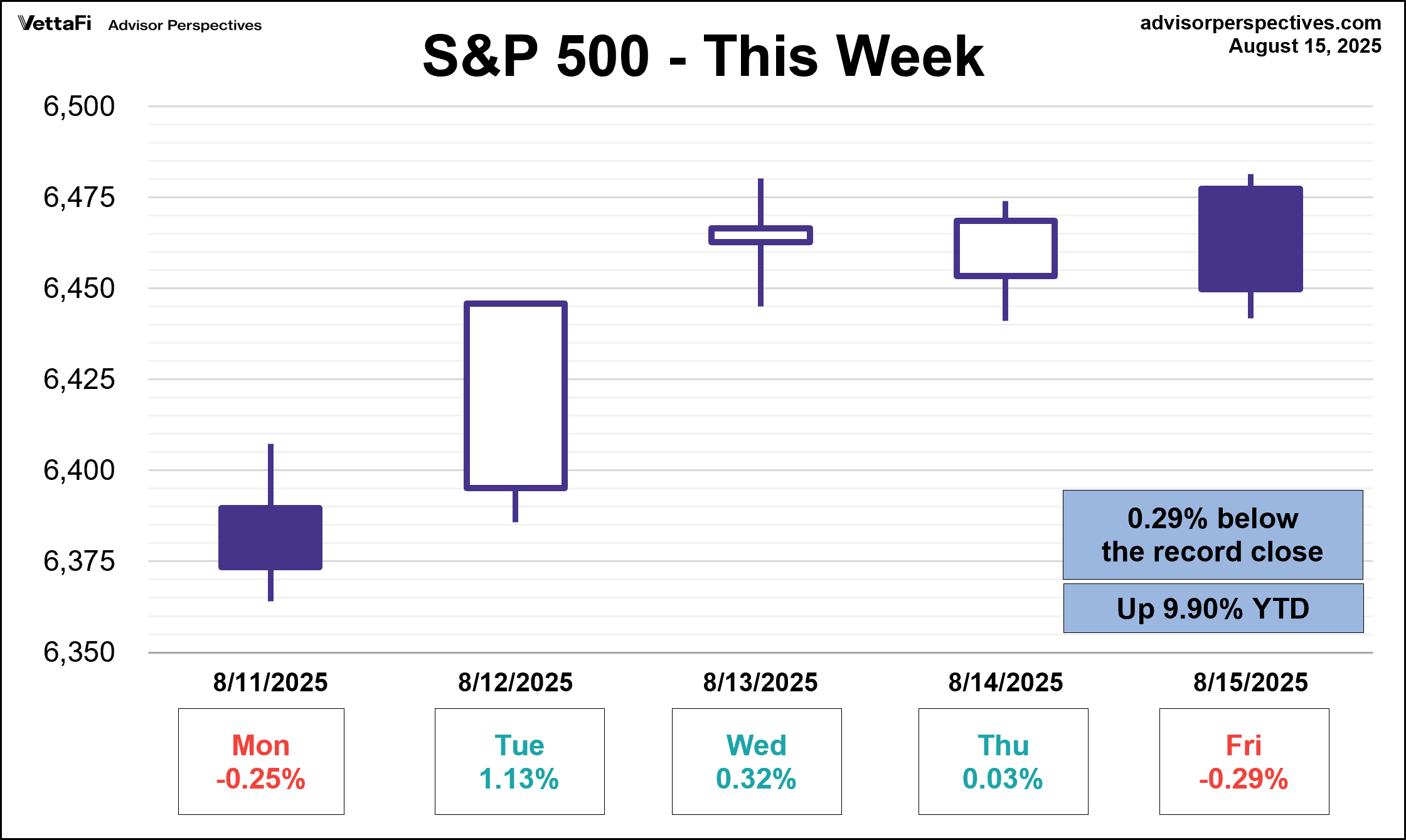

The S&P 500 notched three new record highs last week but the rally fell short on Friday. The index ultimately finished the week up 0.9%, its fourth weekly gain in the past five weeks. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 1.0% last week. Meanwhile, the S&P Equal Weight Index was up 1.5% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) rose 1.5%.

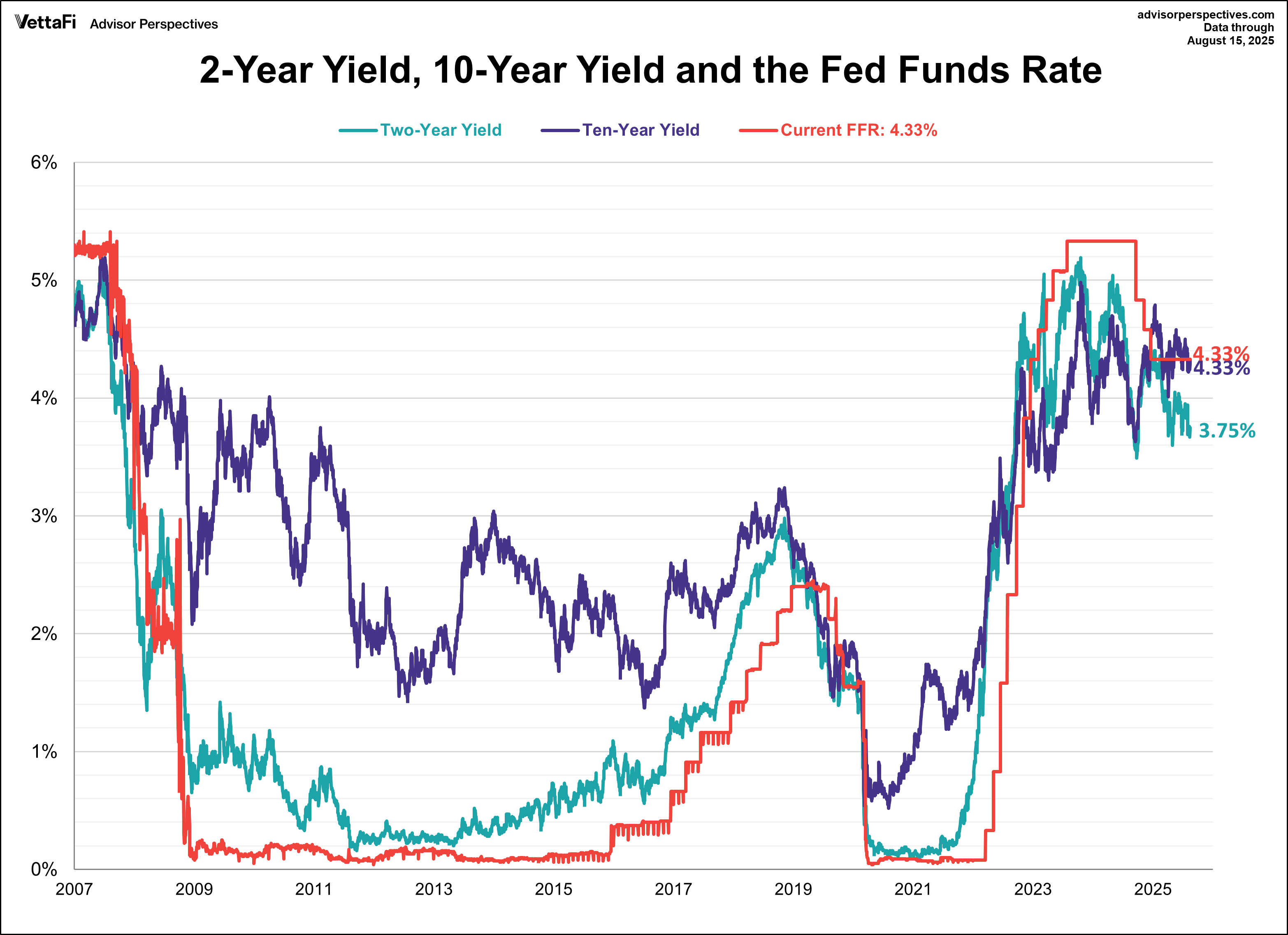

The 10-year Treasury yield finished the week at 4.33%, while the 2-year note finished at 3.75%.

The CME FedWatch Tool currently shows an 85% likelihood that the Fed will cut rates by 25 basis points at their meeting next month. Markets are pricing in another 25 basis point cut at the October meeting and three additional cuts in 2026.

Economic Data in the Week Ahead

The week ahead will provide a fresh look into the housing market and monetary policy. Key housing data will be in focus with the release of Housing Starts, Building Permits, Existing Home Sales, and the Zillow Home Value Index, which will shed light on the state of the real estate market. In manufacturing, the Philadelphia Fed Manufacturing Index will be published, offering a look at regional factory activity. Finally, central bank watchers will be paying close attention to the Fed Meeting minutes from the July FOMC meeting, as well as the start of the Jackson Hole Symposium, which often features significant speeches from Fed officials.

Membership required

Membership is now required to use this feature. To learn more:

View Membership BenefitsSponsored Content

Editorial Calendar

View Full Calendar Eastern Time Zone

+ Add the editorial calendar to your Google Calendar.

Upcoming Virtual Events View All