Today, the mission of the CFP Board of Standards, a 501(c )(6) nonprofit organization, is to credential competent and ethical financial planners, uphold CFP® certification as the recognized standard, and advance the financial planning profession. The mission is no longer to benefit the public. Selling out the public dooms financial planning as a profession. That’s horrible for the vast majority of certificants that want to be held to a higher standard.

Before I recommend what to do, I want to first state what not to do. Don’t invest as if you think you know what long-term inflation will be. Will we return to the double-digit inflation of the late ‘70s and early ‘80s? The answer is: Nobody knows.

When it comes to investing, it’s the Wild West out there. Our clients are hearing things from less scrupulous members of the financial services industry that appear true on the surface but are really aimed at separating people from their money.

While artificial intelligence is unlikely to replace financial advisors, it can certainly enhance both the quality and the productivity of advisors who embrace it. I agree that AI will boost productivity, but I wanted to put it through the test now to see how accurate and insightful it was. To do so, I gave Anthropic’s Claude a spin.

It’s human instinct to want to know what the future holds and to protect and grow our nest egg based on our perceived knowledge of the future. It takes courage to ignore those economic forecasts from brilliant, well-meaning experts with very impressive credentials. Their logic is always compelling, but investing based on that logic can be hazardous to your wealth.

Despite having little expertise when it comes to the subject of happiness, I’m fascinated by the subject of money and happiness. In this article, I discuss my own failed experience, review research on money and happiness, and offer my hypothesis on investing and happiness.

Nominal thinking in investing, a form of the "money illusion" bias, is the failure to account for inflation's erosion of purchasing power. The primary problems with this approach are overestimating real returns, misjudging true wealth, and making poor long-term investment decisions based on misleading nominal figures.

Clients with large, concentrated stock positions, often from vested Restricted Stock Units (RSUs), face undiversified risk and a huge potential tax bill. This article introduces two new, complex methods that defer capital gains.

Be wary of claims that indexing and passive investing have huge hidden costs. In my view, passive investing involves owning, as close as is economically feasible, every stock weighted to market capitalization. So this means total stock index funds.

I’m a big believer in simplicity for most things, and that includes investing. When constructing a portfolio, simplicity is what I aim for. In this piece, I offer a brief summary of how I analyze the holdings and make recommendations on what to keep and what to get out of when a client asks me to review and improve their investments.

Clients work a lifetime for financial freedom. Once retirement comes, they often have a large nest egg to spend. However, there can also be a huge fear of spending the portfolio down.

When it comes to investing, I’ve learned that common sense isn’t all that common. In fact, I’ve seen brilliant people lose millions of dollars on investments without using one ounce of common sense.

Here are some brilliantly simple lessons for us all that I learned from Warren Buffett.

The ever-louder brouhaha surrounding BBD is much ado about nothing. It is expensive, dangerous, and likely to benefit only bankers and brokerage firms.

So what has caused such a surge in international returns versus the U.S. so far this year? Is it just short-term noise, reversion to the mean, or something more systematic? If the last few months were purely short-term noise, we will soon know, as U.S. stocks will resume dominance.

On the evening before his presentation at the Exchange Conference last week, I sat down with Rob Arnott to discuss whether now is the time for smart beta to shine. Arnott is the founder and chair of Research Affiliates and is known as the “godfather of smart beta.”

Though you may not agree with my view on all seven of these terms, it may be beneficial for you and your clients to at least consider them.

’ll first summarize their projections and note what I think are some shockers. Then I’ll take a look at how accurate their past forecasts have been. Finally, I’ll conclude with what I’m changing in my own portfolio...

Double-digit increases in rates are common. I’m definitely feeling the pain, as I suspect you are. So here are a few things I do to help my clients save some money.

Rather than go back and reminisce about the articles I’m most proud of, I think a better exercise is to look at those I got wrong and reflect on what might be learned.

Building a TIPS ladder gives us a license to spend and creates a spending floor. My TIPS ladder combined with Social Security provides a $10,000 monthly inflation-adjusted cash flow, though I’m delaying taking Social Security until age 70, of course.

Rules are made to be broken, so I would call this a 50 percent starting place in your discussion with the client. I certainly wouldn’t recommend only a 50 percent equity portfolio to a young client with a high willingness and need to take risk or the same to any client who had a low willingness and need to take risk.

Is this the beginning of the inevitable bear, where these then-most-valuable stocks could get clobbered? Here’s what history teaches us about the current concentrated market and the current correction.

Conflicts are everywhere in financial planning. They exist in all fee models, whether they be commissions, assets under management, fixed fee, or hourly. Any time money changes hands there are conflicts of interests.

With crypto going mainstream, it’s important that advisors understand the pros and cons of including crypto in a portfolio.

Corporate America is buying back its own shares at a near record pace, despite a new one percent buyback excise tax instituted in 2023. While buybacks are often criticized, they are wonderful for investors – though probably not in the way most people think.

The article to which this “Concerned American” refers was about investing in low-cost diversified index funds and U.S. Treasury instruments, such as TIPS. It wasn’t about politics, nor was I even thinking of the election as I wrote the piece.

Implementing the TIPS ladder is clunky, so I challenged the fund industry to simplify and improve with a TIPS ladder Fund. Stone Ridge Asset Management has done just that with its new LifeX Inflation Protected mutual funds.

While investing strategies should be consistent, changes in markets and the economy make some advice more relevant than it was in the past. Here are the top 10 things I’m telling clients.

Beginning this year, the SECURE Act 2.0 allows owners of 529 plans to convert unused 529 funds to the beneficiary’s Roth IRA.

If you own bond funds in a taxable account, it is possible to turn some of the SEC yield into long-term capital gains taxed at lower rates, which could save a bundle. Here’s how.

Passive investing means buy and hold, and that’s not what I do for my own portfolio or recommend to clients. Here are eight ways I’m an active investor.

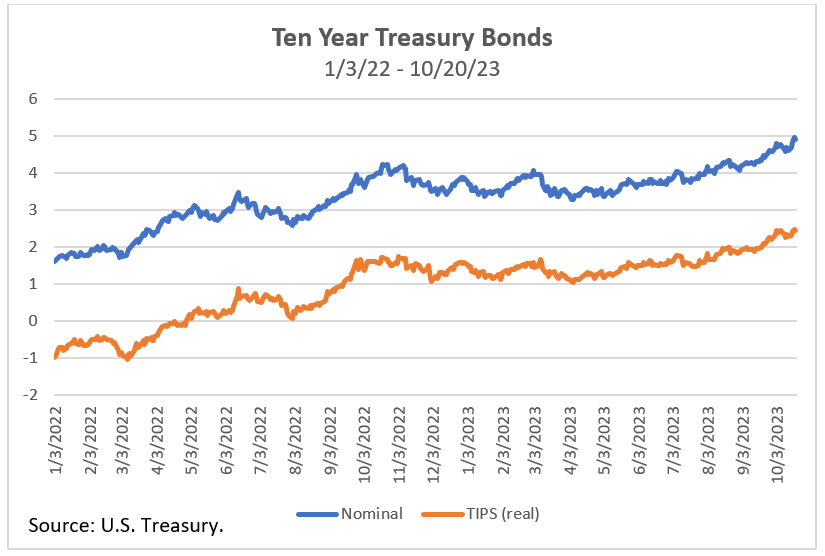

Let’s examine what the bond market is telling us about inflation and a solution that will pay you and your clients to insure for the possibility of continued high, long-term inflation.

When it comes to the “art” of convincing people to buy services or products, I consider myself the worst salesperson on the planet.

Here’s how I apply behavioral finance to help clients to think differently about their investing.

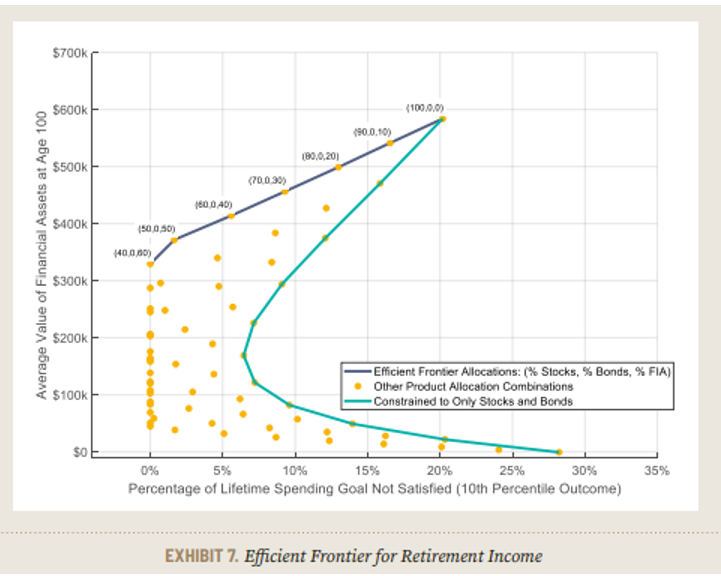

When adjusting for more realistic assumptions and considering the fact that the insurance company can change return caps and that inflation is both an unknown and deep risk, an FIA, along with most annuities, is not on the efficient frontier in either accumulation or decumulation phases.

As we enter the hurricane season, there are signs of three financial calamities merging to form the perfect storm. The nexus is in commercial real estate, but it extends to banking and the broader economy.

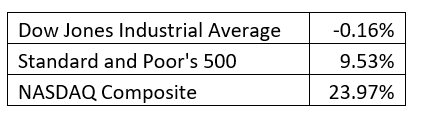

How have U.S. stocks performed this year? The answer is simple, but you’d never know that from looking at the three most often quoted indexes.

AI’s arrival will have an increasingly large impact on our lives. That includes investing and, especially, other aspects of financial planning.

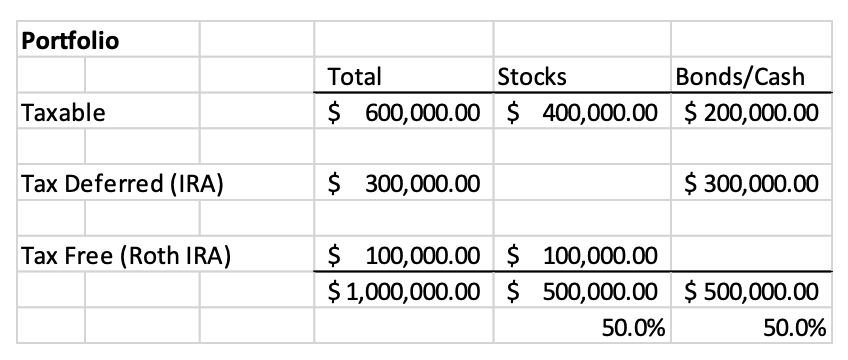

One of the toughest dilemmas I wrestle with is whether to consider future tax liabilities from unrealized gains in the portfolio and taxes from withdrawing from traditional retirement accounts.

Here is some research on why our clients built a sizable portfolio while others had high income but little savings. I’ll address specifics on how to get savers to enjoy their money.

Over the past couple of decades, I’ve told clients many very important things. Most of them are timeless, which is why I find myself saying the same things repeatedly. Here are the top 10, and I’ve saved my most important for last.

Morningstar’s latest research showed higher safe spending rates across all asset allocations over all time horizons. I don’t agree with those results.

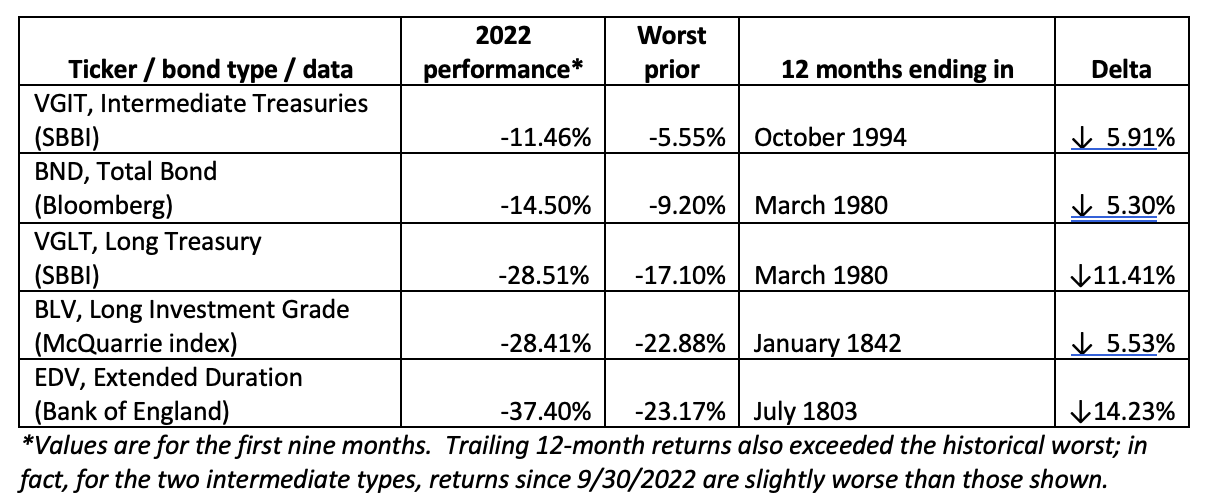

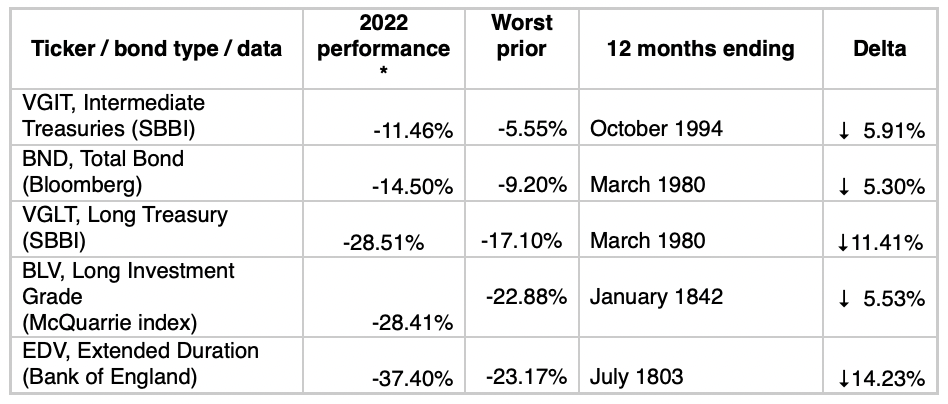

Rising interest rates was the dominant story in 2022. Did fixed income losses cripple insurance companies? Or has the insurance industry shifted the risk to your clients who purchased their products?

I built a 4.36% real (inflation-adjusted) systematic withdrawal portfolio using a 30-Year TIPS ladder.

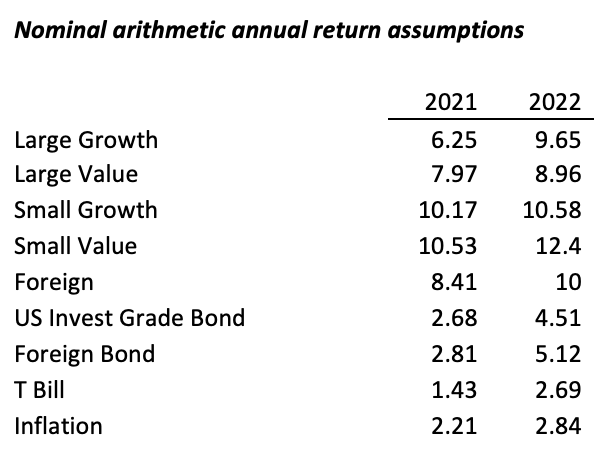

Despite crippling stock and bond market performance in 2022, there are nuggets of good news for clients.

I wrote an article last month regarding the 10 things I got wrong about financial planning over my 20-year career. As it happens, I also got some things right and was happy when I was asked to write about them.

In the last two decades as an investment advisor, I’ve often been wrong – about markets, products and their providers, investors, the government, and the advisory business. Here are my top 10 items I’ve got wrong.

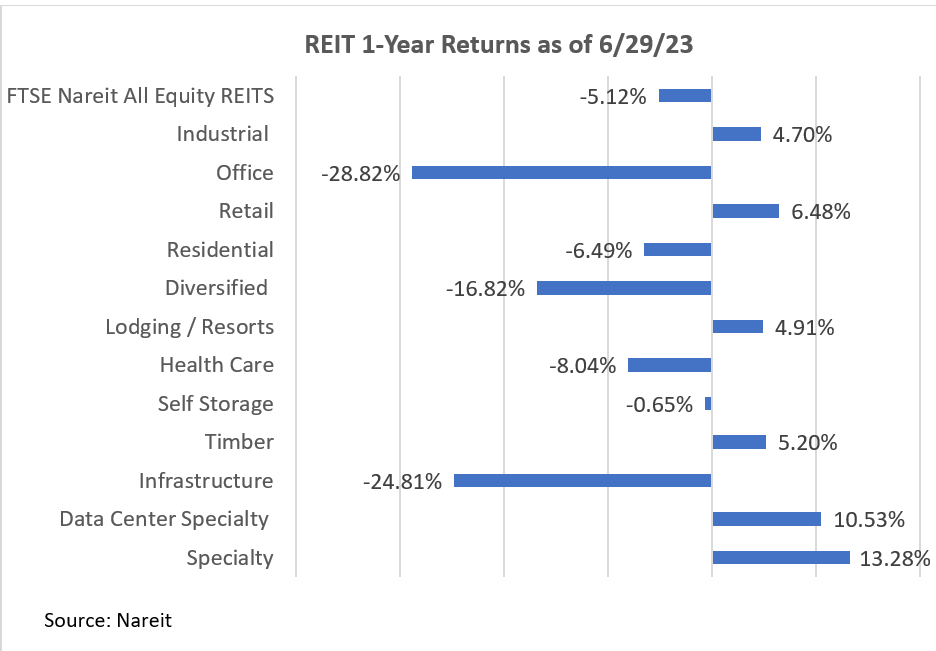

None of us can control markets, but it’s critical that our clients know how they have performed relative to appropriate benchmarks.