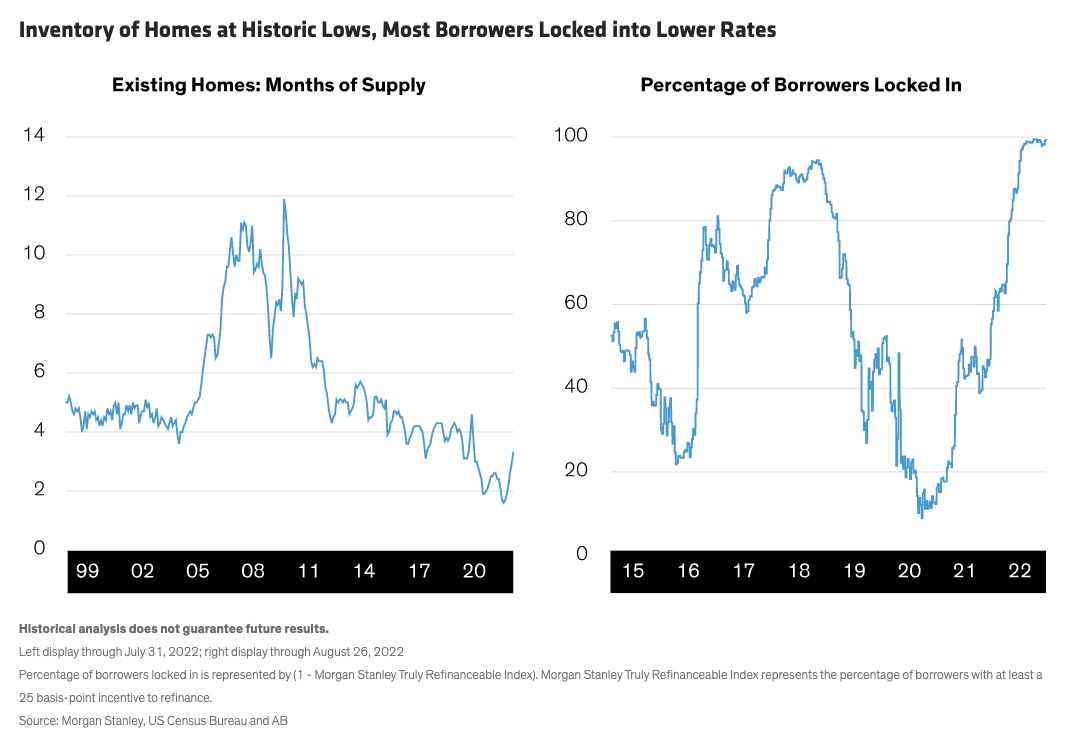

It can sometimes be hard to tell whether the US housing market is hot or cold. Currently, existing-home inventory is tight and prices are stable—indicators of a hot market—while sales volume is down and home price appreciation has slowed. So, what’s the temperature?

By contrast with traditional discretionary approaches, systematic fixed-income models are exclusively data-driven and operate autonomously—ranking securities, constructing optimized portfolios and managing risk without traditional inputs or discretionary overlays.

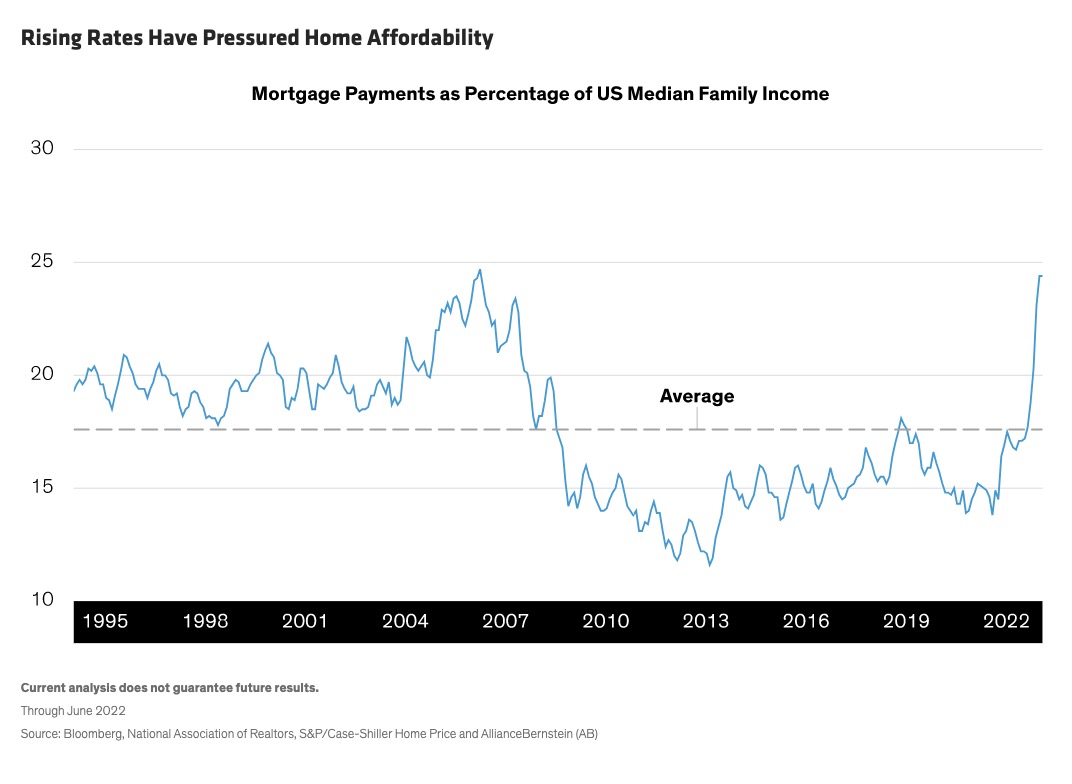

Over the last few years, the US housing market has defied expectations as prices, helped by constrained supply, have remained resilient—despite high mortgage rates and affordability challenges for homebuyers. But the outlook appears to be darkening, with recent headlines seizing on potentially adverse trends.

As investors re-evaluate their allocations to US assets, we think they should consider euro-denominated bonds.

Building a bond portfolio these days isn’t easy. Interest rates have been volatile. Credit spreads are tight. And sweeping change in US fiscal, trade, and regulatory policy is underway. We think securitized assets deserve a closer look.

We demystify the credit risk transfer securities market.

Investors who wait too long to get off the sidelines may find they’ve missed out.

The 10-year Treasury yield has climbed steadily over the past two years. But we believe fixed-income investors should be prepared for lower yields ahead.

The pandemic hurt small retailers by hastening the transition to digital commerce and emptied office buildings by turning living rooms into workspace. But it also fueled a warehouse building boom and unleashed a torrent of pent-up travel-and-leisure spending when economies reopened, underscoring the diversity of commercial real estate.

With interest rates on the rise, the once red-hot US housing market is finally showing signs of cooling.

One of the most crucial components of investing in commercial mortgage-backed securities (CMBS) is assessing the underlying collateral value. But what if investors are disregarding risks that threaten a property’s very existence?

Even with today’s low yields, credit barbell strategies can still meet their objectives of downside protection, upside participation and efficient income.

As fixed-income markets have started to recover following the massive selloff and liquidity crunch in March, credit risk-transfer securities (CRTs)―agency mortgage securities not guaranteed by Fannie Mae and Freddie Mac―have been slower to do so. Investors are wondering: Where do CRTs go from here?

Trade tensions—and the volatility they bring—are forcing investors to think about new ways to generate low-volatility income. A mortgage income strategy that balances high-quality securities with historically high-returning ones can help.

The median price of a US single-family home has risen just over 40% since the last housing-market crash. While newspaper headlines may put readers on edge, our analysis indicates a gradual slowdown, not a bursting bubble—in most regions.

Bond investors get anxious when rates rise suddenly, as Treasury yields have recently. But if your investment horizon is longer than a few months, rising rates are nothing to be afraid of.

Investors seeking floating interest-rate exposure and high yields are increasingly turning to credit risk–transfer securities (CRTs), a fairly new type of mortgage-backed bond. But could US tax-code changes hurt the housing market and, by extension, CRTs? We don’t think so.