Last week’s economic narrative centered around the Federal Reserve's latest rate cut, a decision complicated by the government shutdown and lack of economic data. Other reports from the week showed a third straight drop in consumer confidence and a continued slowdown in U.S. home prices. Meanwhile, the S&P 500 reached a record high early in the week, even crossing the 6,900 milestone in intraday trading. Bond markets, however, offered a cautionary counterpoint, pushing Treasury yields to multi-week highs in reaction to the Fed’s outlook.

Federal Reserve Meeting: October 29, 2025

The Federal Reserve implemented a widely anticipated 25 basis point rate cut last week, adjusting the federal funds rate to a new range of 3.75-4.00%. This marks the second consecutive rate reduction and places the central bank’s target at its lowest level since December 2022. This decision came under unique circumstances, as the ongoing government shutdown meant policymakers were forced to make this critical adjustment while essentially flying blind regarding key economic data.

While Fed Chair Jerome Powell has emphasized that another cut in December is not “a foregone conclusion,” the CME FedWatch Tool currently indicates a 65% likelihood that the Fed will continue cutting rates, compared to a 35% likelihood rates will hold steady. However, markets have recently pulled back their longer-term expectations, now projecting only two additional 25 basis point cuts for 2026 and none in 2027.

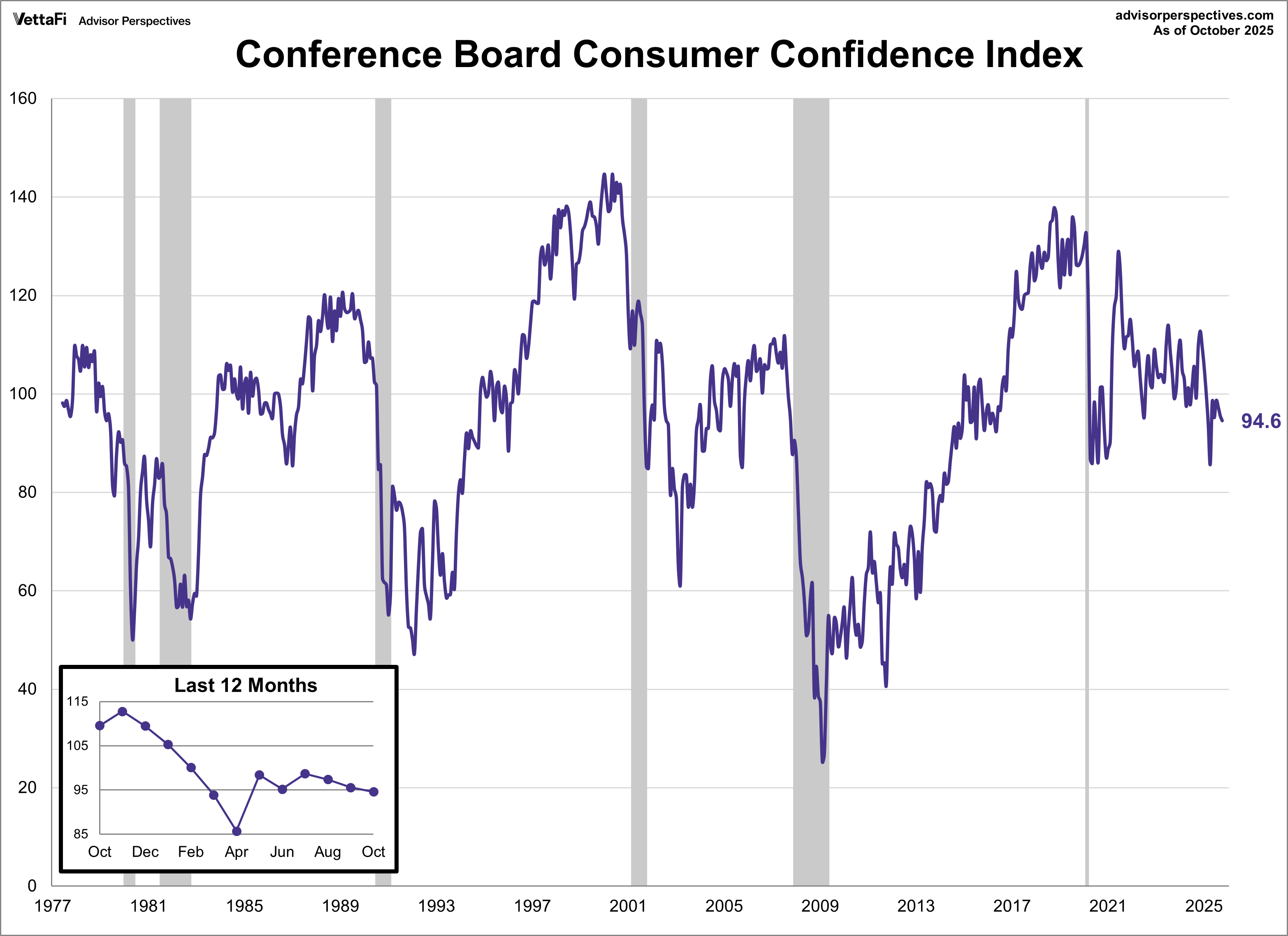

Conference Board Consumer Confidence Index

Consumer confidence fell for a third straight month in October, with the Conference Board Consumer Confidence Index® dropping 1.0 point to 94.6. While this reading was slightly higher than the expected 93.4, it keeps the index at its lowest level since April. This overall decline was driven by weakness in future expectations, which was mostly offset by improved view on current conditions

On the present side, consumers' views on current job availability improved for the first time this year, and their assessments of business conditions also edged upward. However, all three components of the Expectations Index weakened. Consumers continued to express pessimism about future job availability and business conditions, while optimism regarding future income retreated. The survey also revealed that inflation and higher prices remain the chief concerns influencing consumers' views, with 12-month inflation expectations inching up from 5.8% to 5.9%.

The Consumer Discretionary Select Sector SPDR ETF (XLY) is tied to consumer confidence.

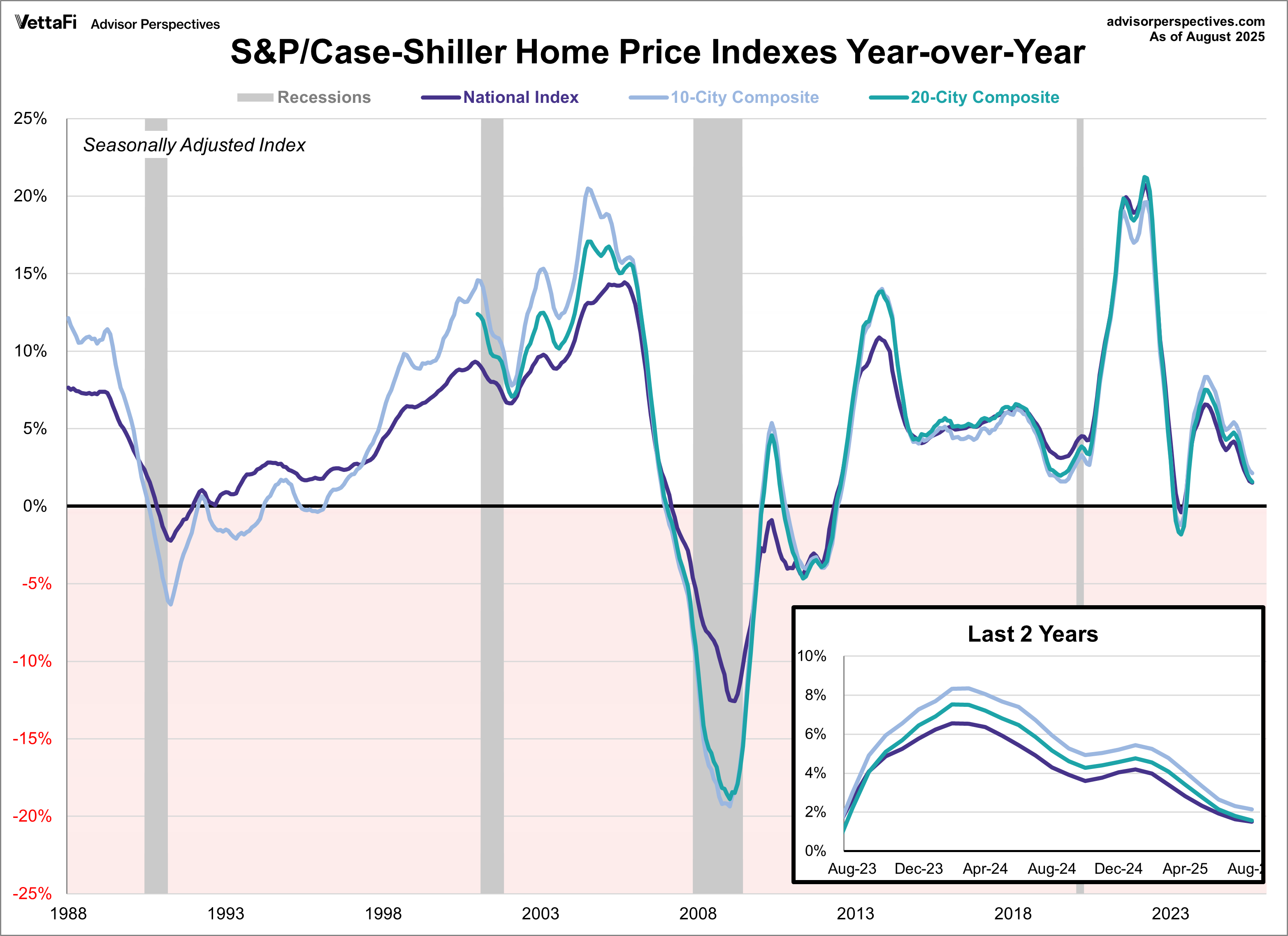

S&P CoreLogic Case-Shiller Home Price Index

The S&P CoreLogic Case-Shiller Home Price Indices, a benchmark for U.S. housing prices, indicated that home price appreciation continued to slow in August. All three major indices, the National, the 20-city, and the 10-city, registered their first monthly gain since February by rising 0.2% from the previous month. Specifically, the National Home Price Index rose 1.5% year-over-year, the 20-city index increased 1.6% annually, and the 10-city index saw a 2.1% annual gain.

Despite the monthly uptick, August marked the seventh straight month that annual gains have slowed, resulting in the smallest annual increase for all three indices in over two years. The persistence of elevated mortgage rates and home prices remaining near record highs has created significant affordability challenges. This sustained pressure on buyers has ultimately led to limited overall market activity.

The home price index could impact the Shares Residential and Multisector Real Estate ETF (REZ).

Market Reactions

The S&P 500 finished the month of October on a positive note, ultimately finishing up 2.3% from September. The index posted a weekly gain of 0.7%, its fourth in the past five weeks. As a result, the SPDR S&P 500 ETF Trust (SPY) rose 0.7% last week. Meanwhile, the S&P Equal Weight Index was down 1.8% from the previous week and the Invesco S&P 500® Equal Weight ETF (RSP) fell 1.7%.

The 10-year note jumped to its highest level in nearly three weeks while the 2-year note climbed to its highest level in over a month last week. The yield on the 10-year note finished the week at 4.11% while the 2-year note ended at 3.60%.

Economic Data in the Week Ahead

Typically, the most anticipated news of the first week of a new month is the jobs report from the Bureau of Labor Statistics. However, the ongoing government shutdown continues to delay this, along with other critical pieces of data. Therefore, the ADP National Employment Report for October will fill in as the primary indicator for the labor market this week.

Other noteworthy releases will offer further insights into the economy. These include the Manufacturing and Services PMI readings from S&P Global and the Institute for Supply Management, which will offer a glimpse into the economic activity of both sectors. Additionally, the University of Michigan’s Consumer Sentiment Index will provide a timely pulse check on consumer attitudes toward the economy.

Read more commentaries by VettaFi | Advisor Perspectives